I haven’t been to the US in more than ten years, but if you looked at my finances today, you might think I live there. I get paid in dollars, keep a dollar account, save in dollars, and use platforms that charge (you guessed it) in dollars.

At some point it becomes obvious: having a dollar card will make everything easier.

This is the reality for millions of freelancers, remote workers, online entrepreneurs, and global teams today. They may live in Brazil, India, Nigeria, Kenya, or the Philippines, but their financial lives often revolve around the US dollar.

In this guide, I’ll explain what a virtual USD card is, how non-US residents can get one, how much they cost, and why they have become one of the most practical financial tools for people working globally.

A virtual dollar card is a digital card that lets you spend in US dollars online.

Instead of receiving a plastic debit or credit card in the mail, you receive digital card details that include the card number, expiration date, and CVV security code. These details can be used immediately to shop online and pay bills.

The key difference between a virtual dollar card and a regular bank card is the currency. A virtual USD card is denominated in US dollars, which means payments are processed directly in USD.

This matters because many online services globally priced in dollars. When you try to pay with a local currency card, your bank usually converts the transaction to USD and adds a foreign transaction fee at varying rates. These fees typically range from 2% to 5% per payment, depending on the bank and country.

A virtual dollar card removes that extra conversion step and its added costs. If you already hold funds in USD, you can simply pay directly in dollars.

For people who work online or run global businesses, using a virtual dollar card often becomes the easiest way to manage international expenses.

Also read: How to pay online and in stores worldwide with your phone

Yes. Non-US residents can now get a virtual dollar card even if they do not live in the United States and do not have a US bank account.

In the past, getting a USD debit card usually required opening a bank account with a US bank. This typically involved providing a US residential address, a Social Security Number, and completing identity verification in person. For most people living abroad, this made the process complicated or impossible.

Modern fintech platforms have changed that.

Today, many digital financial services allow users to open multi-currency accounts online, hold balances in USD, EUR, or GBP, and generate virtual cards linked to those balances.

The entire process can usually be completed remotely in a few minutes. These platforms use secure identity verification processes, relying on internationally accepted documents like passports or national ID cards to confirm users before granting access.

As a result, freelancers, remote workers, startups, and global entrepreneurs now have access to USD payment tools that were previously limited to US residents.

One of the biggest misconceptions about USD payment cards is that you need to open a bank account in the United States to get one.

That used to be true. Most US banks require:

If you’re living outside the US, such requirements makes getting a USD debit card incredibly difficult.

Modern fintech platforms have changed that model. Instead of requiring US residency, many providers now offer multi-currency digital accounts that include USD balances and virtual cards. These accounts are regulated financial services that allow users to hold and spend dollars without opening a traditional US bank account.

Getting started is much simpler, but still secure. Verification is completed online through standard KYC checks, using trusted identity documents such as:

These checks help ensure your account is properly verified and protected. Once you’re set up, you can generate a virtual card within minutes and start making payments online.

Yes. Non-US residents generally do not need a Social Security Number to obtain a virtual dollar card.

Instead of using US tax identifiers, most digital payment providers verify identity through international documentation. This usually involves submitting a government-issued ID and completing biometric verification during the account creation process.

The absence of credit checks is another advantage. Because most virtual dollar cards function as prepaid or debit cards, users spend their own balance rather than borrowing money. This means there is no credit history requirement and no risk of accumulating interest or debt.

For freelancers and remote workers who earn internationally, this model makes it much easier to access USD payment tools regardless of where they live.

Not all virtual dollar cards work the same way. Depending on the platform, they can be linked to different types of accounts or balances.

Understanding the difference can help you choose the option that works best for your needs.

Prepaid virtual cards are loaded with a specific amount of money before you use them.

You first add funds to the card, and then spend from that balance until it runs out. Many platforms use this model because it’s simple and easy to control.

Since you can only spend the amount you load, prepaid cards are often seen as a good option for budgeting and security.

Debit virtual cards are connected directly to a balance in your account, usually a USD wallet or multi-currency account.

Instead of loading money onto the card itself, payments are deducted directly from your available balance.

Many fintech platforms, including Grey, issue debit-style virtual cards linked to a USD balance.

Some platforms also offer disposable virtual cards designed for single-use or temporary payments.

These cards are useful when:

Once the payment is completed, the card number is no longer valid.

For most freelancers, remote workers, and global businesses, a debit virtual dollar card linked to a USD balance tends to be the most practical option. It allows you to manage your funds easily while paying for global services, subscriptions, and tools that charge in USD.

Security is one of the main advantages of virtual cards.

Unlike physical cards, virtual cards cannot be lost or stolen. Because they exist only digitally, card details are stored within the user’s account and can be regenerated instantly if necessary.

Most providers also include additional security measures such as two-factor authentication, real-time transaction alerts, and the ability to freeze or unfreeze cards instantly.

Another common feature is 3D Secure authentication, which requires the user to approve certain transactions before they are completed. This helps prevent unauthorised payments even if card details are exposed.

For users who regularly make online purchases, these security features make virtual cards one of the safest payment options available.

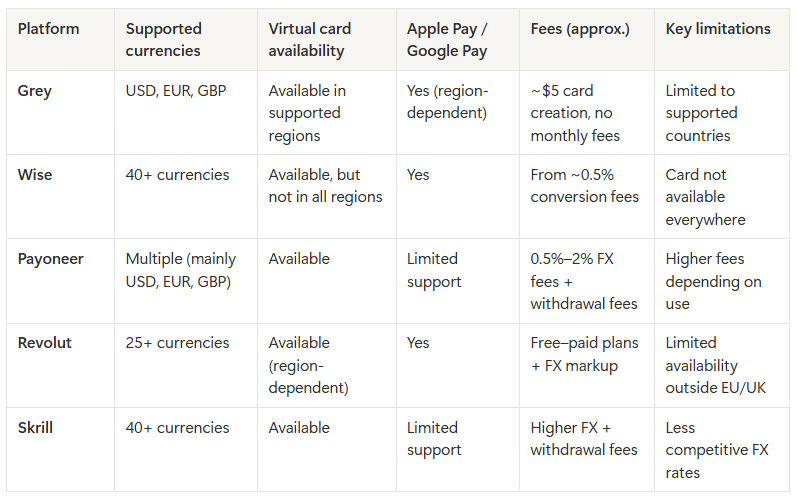

Several platforms now offer virtual cards for international users. While the basic functionality is similar, there are important differences in pricing, supported currencies, and card availability.

Wise, Payoneer, and Grey are three of the most widely used platforms among freelancers and remote professionals.

Each platform serves a different purpose. Wise focuses on global banking, Payoneer is built for marketplace payouts, and platforms like Revolut and Skrill lean more towards digital banking and prepaid payments. Grey is built specifically for freelancers and remote workers who want direct access to multi-currency accounts and fewer barriers when managing international payments.

The best option depends on how you earn, where you live, and which currencies you use most frequently.

If you’re ready to get a virtual dollar card, the process is usually quite straightforward.

With Grey, for example, it only takes a few steps:

Opening an account is done entirely online. After signing up on the Grey website or through the mobile app, users complete a short identity verification process. Once this is complete, you can generate your virtual card directly from the Cards section of the dashboard.

.avif)

The card is issued instantly, and the card details including the card number, expiration date, and CVV become available immediately for online payments. This allows users to start paying for subscriptions, digital services, and international platforms without waiting for a physical card to arrive.

Grey currently charges $5 to create a virtual dollar card, which includes a $4 one-time issuance fee and a $1 minimum funding requirement. Unlike some providers, there are no monthly maintenance fees, so users are not charged simply for keeping the card active.

.avif)

The card is connected to Grey’s multi-currency account, where users can hold balances in USD, EUR, GBP and NGN. If a USD balance is already available, payments are deducted directly from there. If not, funds can be added by converting another supported currency. The exchange rate is shown before confirming the conversion, so users can see the exact amount they will receive.

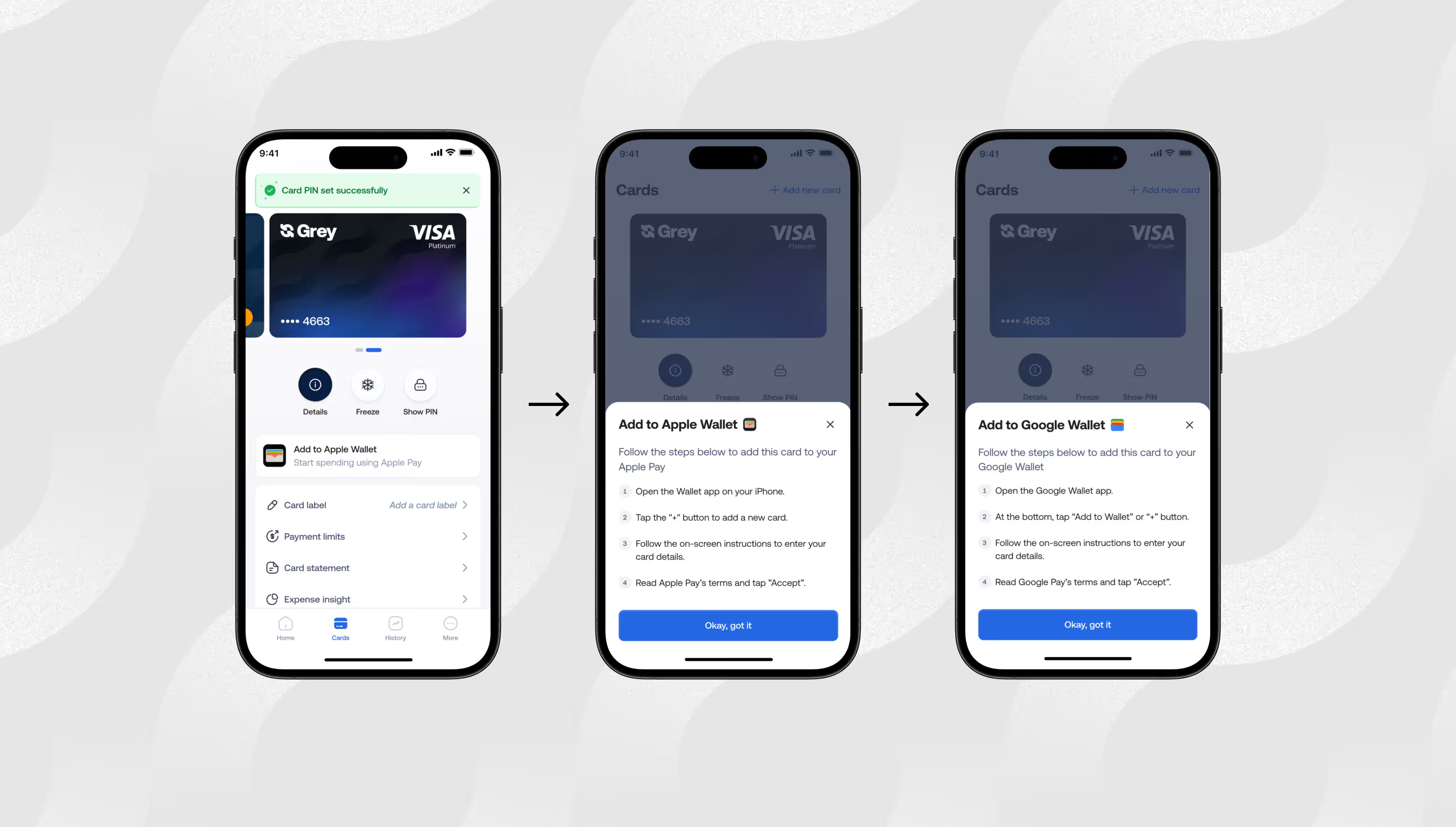

Although the card is virtual, it is not limited to online payments. In supported regions, the Grey virtual card can be added to Apple Pay or Google Pay, allowing users to make contactless payments in physical stores using their phone. This makes it possible to pay for everyday purchases from the same USD balance used for online services.

Also read: How to add your Grey card to Apple Pay or Google Pay

Security is another key feature of virtual cards. Payments are protected by 3D Secure authentication, which requires confirmation before certain transactions are completed. Users can also freeze or unfreeze their card instantly from the app if they suspect suspicious activity.

And that’s it. Once the card is created, you can use it to pay for online services, subscriptions, international platforms and contactless payments.

In most cases, the entire card creation process can be completed online in minutes.

Also read: Grey card vs other virtual cards: what you should know

Open your Grey account, fund your USD balance, and create your Grey virtual card to start paying for global services in minutes.

Yes. Many fintech platforms now offer multi-currency accounts that allow non-US residents to generate virtual dollar cards without needing a US bank account or US residency.

Most platforms issue virtual cards instantly once identity verification is completed. The entire process usually takes less than 10 minutes.

Users typically need a government-issued ID such as a passport or national identification card. Some providers may also require proof of address.

Yes. Virtual cards can be used for most recurring payments, including streaming services, SaaS subscriptions, cloud hosting platforms, and digital tools.

Spending limits vary by provider and account level. Many cards allow daily transactions between $500 and $5,000, while higher limits may be available after additional verification.

Some providers, like Grey, support mobile wallets, allowing users to make contactless payments with their phones even without a physical card.

.svg)

Back to top