If you live in India and earn, plan to earn, or want to invest in US dollars, you’ve probably searched:Can I open a US bank account from India?

Do I need a US address?

Can I open a US account without an SSN?

Is there a way to receive USD without high fees?

Let’s answer this clearly.

Yes, it’s possible to get access to US banking details from India without flying to the United States. But the method you choose determines how complex, expensive, or practical it will be.

Here’s what actually works in 2026.

TL;DR

You can get US banking details from India without visiting the US, without an SSN, and without a US address. If you're a freelancer or remote worker who just needs to receive USD, you probably don't need a traditional US bank account at all. A fintech platform like Grey gives you a US account and routing number, supports ACH payments, and sets up in minutes. Get started here.

Also read: How freelancers in India can receive payments from the US, UK & EU clients

Opening a US bank account from India usually comes down to one of these reasons:

India has one of the largest overseas populations in the world, with millions of Indians living and working abroad. But in recent years, you no longer have to leave India to build an international career. With global companies increasingly open to remote hiring, more professionals are earning in USD while staying at home.

A US account makes it easier to receive ACH payments, get paid like a local in the US, avoid expensive SWIFT transfer fees, and access USD-based financial services without unnecessary delays or complications.

Traditional US banks are built with US residents in mind, which makes opening an account as a non-resident significantly more complex.

You may also like: How to create US and UK bank accounts as a migrant worker in India

Yes. But not all “US accounts” are the same.

There are two main categories:

Understanding the difference is critical. Many people searching “open US bank account from India without SSN”, “US bank account for non-residents”, or “open US bank account from India without visiting” are actually looking for a way to receive USD payments easily. In many cases, that solution does not require a traditional US bank account at all.

Let’s clear up a few common misconceptions:

Myth 1: You must visit the US

Many digital providers allow fully remote setup.

Myth 2: You need an SSN

Traditional banks do. Many fintech platforms don’t.

Myth 3: You need a US address

Some banks require one. Others accept international applicants.

Myth 4: It takes months

With the right provider, it can take days.

Choosing the right route makes all the difference.

Worth a look: Top platforms to earn US dollars in India

There are three realistic routes.

1. Through Indian banks with US partnerships

Some Indian banks help you open a linked US account. This route may feel familiar but often requires higher balances and longer processing times.

2. Apply directly to a US bank as a non-resident

Some US banks allow international applicants. You may need a passport, ITIN, proof of income, and sometimes a US mailing address. This route works best if you’re relocating permanently.

3. Use a fintech platform that provides US banking details

This is the most practical solution for freelancers and remote workers. Platforms like Grey provide a US account and routing number, allow ACH payments, and complete onboarding entirely online.

If your goal is simply to receive USD efficiently, this is usually the fastest and simplest option.

To give you a sense of scale, thousands of Indian freelancers and remote professionals have used Grey to open USD accounts and receive payments internationally. Many complete onboarding in under 20 minutes — far faster than traditional banking alternatives that can take weeks or months.

That speed and accessibility matter because the world of cross-border work is growing rapidly. Outward remittances under the Liberalised Remittance Scheme (LRS) (including payments for education, freelancing, travel, and services) have been expanding year over year, reflecting the rising number of Indians earning and spending abroad. Referencing this growth helps anchor how relevant cross-border finances are to your career and income goals.

Here’s what the process typically looks like, especially if you choose a digital solution.

Look for providers that explicitly allow Indian residents to open USD accounts remotely. Check whether they support ACH payments and provide US account and routing numbers.

Confirm whether an SSN, ITIN, or US address is required. Many digital platforms do not require these.

You’ll usually need:

Traditional banks may require additional documentation such as tax forms or income proof.

Fill in your personal details, upload documents, and submit verification. With fintech platforms, this is fully online and often takes minutes to complete.

Approval times vary. Traditional banks can take weeks. Digital platforms are often much faster.

Once approved, you may need to fund the account. After that, you can start sharing your US account details to receive payments.

You might find this useful: Getting paid from Europe and the US while living in India

If you’re earning in dollars from India, opening a US bank account sounds like a big step.

But what really matters is how it would change the way you get paid, convert money, and manage your earnings.

Before:

Your client asks for US bank details. You scramble. You consider PayPal. You worry about fees. You lose a chunk of your earnings in hidden conversions.

With Grey:

You get US account and routing numbers in your name, fully online, without an SSN or US address. You share those details like any US-based freelancer would. You receive USD like a local, and the money lands in your USD balance.

Before:

Payouts bounce between platforms, gateways, and expensive currency conversions. Your margins quietly shrink.

With Grey:

You receive your USD payouts directly into your USD account. When you’re ready, you convert to INR and transfer to your Indian bank account. Not when a platform decides. When you decide.

That timing control alone can make a difference in how much you actually keep.

Before:

You receive $1,000. You expect ₹X. You get ₹X minus a mystery.

With Grey:

Pricing is transparent and exchange rates are competitive. You see what you’re converting and what you’re receiving. No guessing and no decoding complicated fee structures.

Before:

You use your Indian debit card for SaaS, ads, or hosting. International charges. Extra fees. Declines. Frustration.

With Grey:

You can use a virtual card linked to your USD balance. Pay for software, ads, subscriptions, or global purchases directly in dollars, without unnecessary cross-border charges.

Before:

One app to receive. Another to convert. Another to track. Screenshots everywhere.

With Grey:

You manage your USD balance, convert to INR whenever you want, track transactions, and handle payments in one place. Built specifically for freelancers, remote workers, founders, and online sellers who earn across borders.

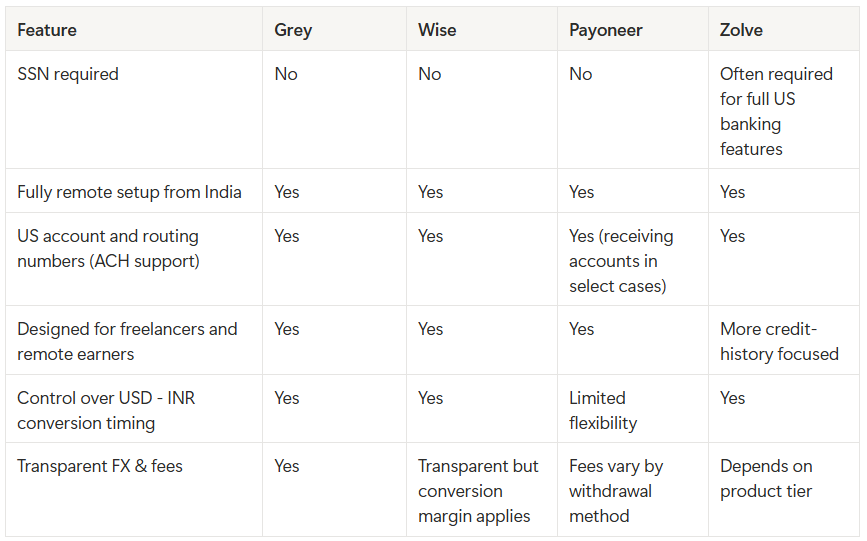

If you’re researching this seriously, you’ve probably come across names like Wise, Payoneer, or Zolve. Here’s a practical side-by-side comparison to help you understand the differences.

Set up your US account details from India in under 10 minutes. Start here.

.svg)

Back to top