If you send money to India from the US regularly, you have probably wondered whether those transfers create any tax obligations. The short answer is that most personal remittances to India are not taxed. The IRS does not treat money sent to family for living expenses, medical bills, or education fees as taxable income for either the sender or the recipient. But there are reporting thresholds, and missing them carries penalties that can dwarf whatever amount you transferred.

A US resident who sends $1,500 per month to a parent in India, totaling $18,000 per year, sits right at the edge of the annual gift tax exclusion for 2024. If you cross that threshold by even a dollar without filing IRS Form 709, you are technically non-compliant. If you hold an NRE fixed deposit in India worth $12,000 at any point in the year, you'll be required to file an FBAR, even if the account balance drops to $500 the next day. When you own Indian mutual funds, you face PFIC reporting that most US tax software does not handle. None of these situations result in a tax bill for most people, but all of them require paperwork, and the penalties for not filing are real.

This guide covers every tax rule that applies when you send money from the US to India: the IRS gift tax exclusion and how it works, FBAR and FATCA reporting requirements, what changes when money is sent for property or investments, how India's own regulations affect US senders, and which scenarios require a tax professional versus which ones you can handle yourself.

Also read: The fastest and easiest ways to send USD from India to the US

The US tax code distinguishes between owing tax and owing a report. Most people who send money to India will never owe gift tax, FBAR penalties, or FATCA fines, as long as they file the right forms. But the forms are not optional, and the penalties for not filing are disproportionate to the amounts involved.

The FBAR penalty for non-willful failure to file is up to $17,000 per account per year. If you have three Indian bank accounts and miss three years of FBAR filings, you could face penalties of up to $100,000, even if the total balance across all accounts never exceeded $15,000. The IRS has enforced these penalties, and courts have upheld them. The point is not to alarm you. It is to explain why a guide like this matters: the cost of compliance is an hour of paperwork. The cost of non-compliance can be catastrophic.

For a US resident who sends $1,000 to $2,000 per month to family in India, the reporting obligations are straightforward once you understand the thresholds. This guide walks through each one in order of the likelihood you encounter it.

Read also: India visa requirements for US citizens

When you send money to someone in India with no expectation of receiving goods, services, or anything of value in return, the IRS classifies the transfer as a gift. Gifts in the US are not taxable to the recipient. The tax obligation, if any, falls on the giver. But for most senders, no tax is owed either, because of the annual exclusion and the lifetime exemption.

The annual gift tax exclusion

The annual gift tax exclusion is the amount you can give to any single person in a calendar year without filing a gift tax return. For 2025, that amount is $19,000 per recipient. The exclusion is per recipient, not per sender. You can send $19,000 to your mother, $19,000 to your father, and $19,000 to your sibling, each separately, without triggering any filing requirement. If you are married and your spouse also sends gifts, each spouse has their own $19,000 exclusion. A married couple can give $38,000 to a single recipient in a single year without reporting.

What counts as a gift: any transfer where you do not receive something of equal value in return. Sending money for rent, groceries, medical bills, school fees, or general support all qualify as gifts. Paying for a family member's flight to visit you qualifies. Sending money to your own Indian bank account does not qualify, because you are transferring to yourself, not making a gift.

What happens when you exceed the annual exclusion

If your gifts to a single recipient exceed $19,000 (or the current year's exclusion) in a calendar year, you are required to file IRS Form 709 (United States Gift and Generation-Skipping Transfer Tax Return) with your annual tax return. Filing Form 709 does not mean you owe tax. It means the amount above the exclusion counts against your lifetime gift tax exemption.

The lifetime gift tax exemption for 2025 is $13.99 million. This is the total amount you can give away over your entire lifetime before any gift tax is actually owed. For most people sending money to family in India, this number is irrelevant in practice. You would need to send $13.99 million in cumulative excess gifts before a single dollar of gift tax is due. But you still need to file Form 709 each year to record the excess. The form is how the IRS tracks your running total against the lifetime cap.

Filing Form 709 is straightforward. You report the total gifts to each recipient, subtract the annual exclusion, and carry the excess forward. Most tax software (TurboTax, H&R Block) supports Form 709. If your situation is simple, meaning regular remittances to family with no property or investment transactions, you can file it yourself.

A practical example

You send $2,000 per month to your mother in India for living expenses. That totals $24,000 for the year. The annual exclusion is $19,000, leaving an excess of $5,000. You file Form 709 and report the $5,000 excess. Your lifetime exemption is reduced from $13.99 million to $13,985,000. No tax is owed. The total time spent on the form: approximately 30 minutes.

If you do not file Form 709, you are technically non-compliant. The IRS may not notice for years, but if you are ever audited, the failure to file creates complications. The fix is simple: file going forward, and consider filing late returns for prior years if the amounts were significant.

Read also: Grey vs. local banks: The best way to exchange currency in India

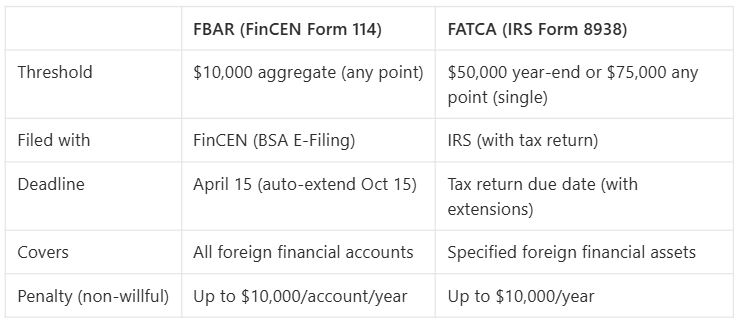

FBAR (FinCEN Form 114, also known as the Foreign Bank Account Report) is a separate obligation from the gift tax. It has nothing to do with how much money you send to India. It is about what accounts you hold outside the US.

The FBAR threshold

If the aggregate value of all your foreign financial accounts exceeds $10,000 at any point during the calendar year, you must file an FBAR. The key words are aggregate (combined across all accounts) and at any point (peak balance, not year-end balance).

Foreign financial accounts include:

How the aggregate rule works

You have an NRE savings account with a balance that peaked at $6,000 during the year, and a fixed deposit worth $5,000. The aggregate peak is $11,000. You must file an FBAR, even though neither account individually exceeded $10,000. If you close the NRE account in March and the balance drops to zero, but the peak was $6,000 in February, the February balance still counts toward your aggregate.

A common mistake: many people think the $10,000 threshold refers to the amount they sent to India during the year. It does not. FBAR is about account balances held, not transfers made. You could send $50,000 to India in a year and have no FBAR obligation if you do not hold any foreign accounts. Conversely, you could send nothing to India and still owe an FBAR if you have old accounts from before you moved to the US.

How to file and deadlines

The FBAR is filed electronically through the BSA E-Filing System (bsaefiling.fincen.treas.gov), not through the IRS. It is due April 15, with an automatic extension to October 15. You do not need to request the extension. It is automatic. The filing takes 15 to 30 minutes if you have your account statements.

Penalties for not filing: up to $10,000 per violation for non-willful failures. Willful violations can result in penalties up to the greater of $100,000 or 50% of the account balance. The IRS has an amnesty program (Streamlined Filing Compliance Procedures) for people who were unaware of the FBAR requirement and can certify that their failure to file was non-willful. If you have unfiled FBARs from prior years, this program is worth investigating before the IRS contacts you.

Also read: How Indians access USD banking without a US address

FATCA (Foreign Account Tax Compliance Act) is a third reporting requirement, separate from both gift tax and FBAR. It requires you to report specified foreign financial assets on IRS Form 8938 (Statement of Specified Foreign Financial Assets), filed with your annual tax return.

FATCA thresholds

FATCA covers Indian bank accounts, Indian mutual funds, stocks held in Indian brokerage accounts, insurance policies with cash value, and other specified foreign financial assets. It does not cover real estate held directly, though rental income from Indian property is reportable on your US return through other forms.

FBAR vs FATCA: do I need to file both?

Possibly. The thresholds are different, the forms are different, and the filing destinations are different. FBAR goes to FinCEN. Form 8938 goes to the IRS with your tax return. If your foreign accounts exceed both thresholds, you file both. The account information is similar, but the forms are not interchangeable.

The rules above cover personal remittances. If you are sending money to India to buy property, invest in mutual funds, or fund a business, additional tax considerations apply. The transfer itself is still not taxable, but the returns on the investment are.

Property purchases

Sending money to India to buy a house, flat, or land is not a taxable event. You are moving your own money to acquire an asset. However, two tax consequences follow:

Indian mutual funds (PFIC rules)

This is where the tax treatment becomes genuinely complicated. Indian mutual funds are classified as PFICs (Passive Foreign Investment Companies) under US tax law. PFIC treatment is intentionally punitive. It was designed to discourage US taxpayers from using foreign funds to defer taxes.

The practical impact: gains from Indian mutual funds can be taxed at the highest marginal income tax rate (currently 37%) plus an interest charge, regardless of how long you held the fund. This is significantly worse than the long-term capital gains rate (0-20%) you would pay on a comparable US-domiciled fund. There are elections you can make (QEF or mark-to-market) to reduce the PFIC burden, but both require detailed annual reporting.

Recommendation: if you are a US tax resident, do not invest in Indian mutual funds without first consulting a tax advisor who understands PFIC rules. The tax cost can easily exceed the investment return.

Fixed deposits

Interest earned on Indian fixed deposits is taxable on your US return as ordinary income, reported in the year it accrues (not the year you withdraw it, if the FD has a multi-year term). India may withhold tax on the interest at source (TDS, typically 30% for NRIs). You can claim a foreign tax credit for the Indian TDS on your US return.

For an NRE fixed deposit, the interest is tax-exempt in India but still taxable in the US. Many NRIs are surprised by this. The Indian tax exemption does not carry over to the US. You report the NRE interest income on your US return and pay US tax on it.

Also read: How to transfer USD from your Indian bank account to a US business partner

No. The Liberalised Remittance Scheme (LRS) is a Reserve Bank of India regulation that limits how much money Indian residents can send out of India. The current cap is USD 250,000 per financial year. LRS applies only to Indian residents sending money abroad. It does not apply to money coming into India from the US or any other country.

If your family member in India wants to send money to you in the US, LRS caps their outbound transfer at $250,000 per year. But if you are sending money from the US to India, LRS is irrelevant. There is no Indian regulatory limit on inbound remittances.

One related rule: if you receive a gift from a person in India valued at more than $100,000 in a calendar year, you must report it on IRS Form 3520 (Annual Return to Report Transactions with Foreign Trusts and Receipt of Certain Foreign Gifts). No tax is owed, but the reporting requirement exists and carries a penalty of up to 25% of the gift amount for failure to file.

The reporting requirements depend on how much you send, whether you hold Indian accounts, and what the money is used for.

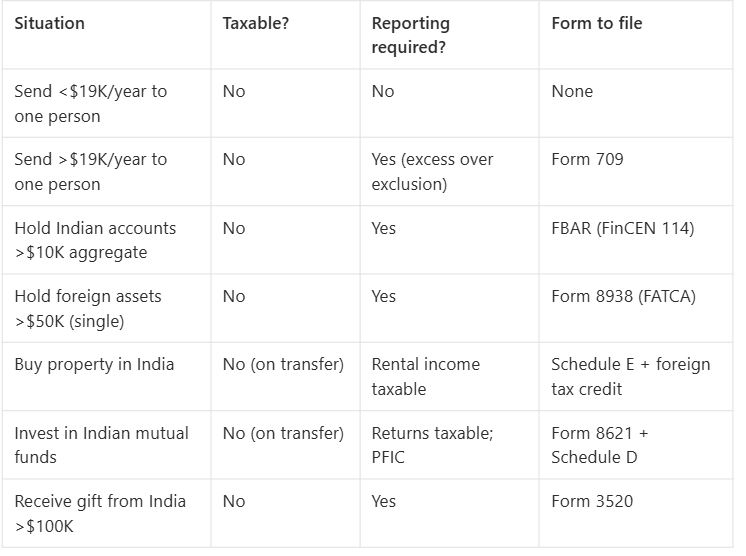

If you send less than $19,000 per year to one person

You are within the annual gift tax exclusion. No Form 709 needed. If you do not hold any foreign accounts above the FBAR threshold, you have zero additional filing obligations beyond your regular tax return.

If you send $19,000 to $50,000 per year to your family

You likely need to file Form 709 for the excess over $19,000. If you hold Indian bank accounts with aggregate balances over $10,000, you also file an FBAR. Both are straightforward and can be done without a tax professional for simple cases.

If you hold Indian investments (mutual funds, stocks, property)

You need a tax professional. PFIC rules for mutual funds, capital gains treatment for property sales, and the interaction between US and Indian tax treaties require expertise that most tax software does not handle. The cost of a CPA who understands cross-border India-US tax issues is $500 to $1,500 per year. The cost of getting it wrong is multiples of that.

If you are unsure whether you are compliant for prior years

Look into the IRS Streamlined Filing Compliance Procedures. This program allows you to file delinquent FBARs and amended returns for the past three years (six years for FBARs) without penalties, as long as your non-compliance was non-willful. The program is straightforward for simple cases, but if the amounts are large or the situation is complex, use a tax professional to handle the submission.

1. Is sending money to India from the US taxable?

Most personal remittances to India are not taxable. The IRS generally treats money sent to family for living expenses, medical bills, or education as gifts, which are not taxed unless they exceed the annual gift tax exclusion ($19,000 per recipient in 2025). If you exceed the exclusion, you may need to file Form 709, but you typically still owe no tax because the excess amount counts against your lifetime exemption of $13.99 million. The transfer itself is not taxed. Only the reporting requirement changes.

2. How much money can I send to India without paying tax?

There is no US government limit on how much money you can send to India. You can send up to $19,000 per recipient per year without triggering gift tax reporting requirements. Above that amount, you may need to file Form 709, but you generally owe no tax unless your cumulative lifetime gifts exceed the $13.99 million lifetime exemption. The IRS does not place a cap on the amount of money you can transfer internationally.

Separately, certain transfers above $10,000 may trigger Currency Transaction Reports under the Bank Secrecy Act. These are informational filings handled by financial institutions and are not tax obligations for the sender.

3. Do I need to file an FBAR if I send money to India?

FBAR is triggered by holding foreign accounts, not by sending money. If the aggregate value of all your foreign financial accounts (Indian bank accounts, NRO, NRE, fixed deposits) exceeds $10,000 at any point during the year, you must file an FBAR regardless of whether you sent any money that year. If you do not hold any foreign accounts, sending money to India does not create an FBAR obligation. The $10,000 threshold is per-person across all accounts, not per-account.

4. What is FATCA and does it apply to my Indian accounts?

FATCA requires US taxpayers to report foreign financial assets above $50,000 (year-end, for individuals filing singly) or $75,000 (at any point during the year) on IRS Form 8938. It covers Indian bank accounts, mutual funds, brokerage accounts, and insurance policies with cash value. It does not cover real estate held directly. FATCA is filed with your tax return, unlike FBAR which goes to FinCEN separately. You may need to file both if your accounts exceed both thresholds.

5. Are Indian mutual fund investments taxable for US residents?

Yes. Indian mutual funds are classified as PFICs (Passive Foreign Investment Companies) under US tax law. Gains can be taxed at the highest marginal income tax rate (37%) plus an interest charge, which is significantly worse than the long-term capital gains rate on US funds. There are elections (QEF, mark-to-market) that can reduce the burden, but they require detailed annual reporting. The tax complexity and cost usually outweigh the investment benefits. Consult a tax advisor before investing in Indian mutual funds from the US.

6. Does India's LRS limit affect me sending money from the US?

No. The Liberalised Remittance Scheme (LRS) governs outbound transfers from India by Indian residents, with a current cap of USD 250,000 per financial year. It does not apply to inbound transfers. If you are a US resident sending money to India, LRS does not restrict or affect your transfers. There is no Indian regulatory limit on the amount of money that can be received from abroad.

7. What if I have not been filing FBARs for previous years?

Look into the IRS Streamlined Filing Compliance Procedures. If your failure to file was non-willful (you did not know about the requirement), you can file delinquent FBARs for the past six years and amended tax returns for the past three years without penalties. The program requires a certification of non-willfulness. For simple cases (small account balances, straightforward situations), you can handle it yourself. For larger amounts or complex situations, use a tax professional.

8. Do I need a tax professional for India-US transfers?

For simple cases (regular remittances to family, no Indian investments, no property), you can handle the filings yourself. Form 709 and FBAR are straightforward. If you hold Indian mutual funds, own property that generates income, or have complex cross-border financial arrangements, you need a CPA or tax advisor who understands both US and Indian tax law. The cost is typically $500 to $1,500 per year. The cost of getting PFIC reporting wrong is significantly higher.

Grey shows the exchange rate and fee before every transfer. No hidden markups, no post-confirmation surprises. Send money to India from the US at grey.co/send-money/us/india.

.svg)

Back to top