When a US resident is sending $1,000 to India, the recepient can get anywhere from INR 83,000 to INR 85,000, depending on which provider they use. That is a $20 to $24 difference per transfer. Over 12 months of monthly remittances, the gap widens to $240-$288. The provider you choose matters more than you think, and the one with the lowest advertised fee is often not the cheapest.

The reason is that most providers earn revenue from two sources: a visible transfer fee and a hidden margin built into the exchange rate. A provider advertising zero fees can cost you more than one charging $5, if the zero-fee provider marks up the exchange rate by 1.5%. On $1,000, a 1.5% rate markup costs $15, three times more than a $5 flat fee. But the rate markup is invisible unless you know how to spot it.

This guide explains what the mid-market rate is and why it matters; how providers structure their pricing to obscure the true cost; a step-by-step method for calculating the real cost of any transfer; and worked examples comparing Grey, Wise, Remitly, and Western Union for real dollar amounts. If you send money to India regularly, this is the single most valuable thing you can learn to reduce your costs.

Also read: How to avoid FX losses as a freelancer in India

The mid-market rate (also called the interbank rate, spot rate, or real rate) is the midpoint between the buy price and sell price of a currency on the global foreign exchange market. It is the rate that banks use when trading currencies in bulk. Reuters and Bloomberg publish it continuously. Google and XE show it when you search for USD to INR.

No consumer transfer service gives you the exact mid-market rate for free. The mid-market rate is a wholesale rate, and there is always a cost somewhere to move money internationally: currency conversion, settlement infrastructure, compliance checks, and profit margin for the provider. The question is not whether you pay something above the mid-market rate. It is how much you pay and whether you can see it.

The mid-market rate is your benchmark. When any provider shows you an exchange rate for USD to INR, compare it to the mid-market rate at that moment. The difference between the two is the markup the provider is charging you, whether they call it a fee, a margin, a spread, or nothing at all.

How to check the mid-market rate

Google "USD to INR". The mid-market rate is updated every few minutes during trading hours. XE.com shows the same rate with more decimal precision. Both are free and accessible from any device. Check the mid-market rate at the same time you check a provider's rate, because forex rates move throughout the day.

Also read: Best way to receive US dollar payments in India

There are three pricing models in the market. Understanding which model each provider uses is essential to comparing them fairly.

Model 1: Visible fee, mid-market rate

The provider charges a fee you can see (e.g., $4.99) and gives you the mid-market exchange rate with no markup. The fee is the entire cost. Wise uses this model. If the mid-market rate is 85.00 and Wise shows you 85.00 with a $4.99 fee, you know exactly what the transfer costs: $4.99.

This is the most transparent model because the cost is a single visible number. You can compare it against any other provider by checking what you would receive net of the fee.

Model 2: No fee, rate markup

The provider advertises zero fees but marks up the exchange rate. If the mid-market rate is 85.00, the provider offers 83.50. The 1.50 INR per dollar difference is the provider's margin. On $1,000, you receive INR 83,500 instead of INR 85,000. The hidden cost is INR 1,500, equivalent to approximately $17.65. You paid no fee, but the transfer cost you $17.65 in rate markup.

This model is less transparent because the cost is invisible unless you compare the provider's rate to the mid-market rate yourself. Many zero-fee providers rely on customers not making this comparison. Western Union and Xoom use variations of this model.

Model 3: Fee plus small rate margin

The provider charges a visible fee and applies a small margin to the rate. Grey uses this model: you see the fee and the rate separately before you confirm. The rate is competitive (close to mid-market) but may not be the exact mid-market rate. The total cost is the fee plus whatever margin exists in the rate.

This model is transparent when both numbers are shown upfront, which Grey does. You can still compare it against any other provider by checking the total INR delivered.

Also read: Top platforms to earn US dollars in India

This four-step method works for any provider, any amount, any day. It takes two minutes and eliminates all the ambiguity in comparing transfer costs.

This method captures both the fee and the rate spread in a single number. It is the only way to compare a zero-fee provider against a fee-charging provider on equal terms.

Also read: How to receive money from UK clients in India

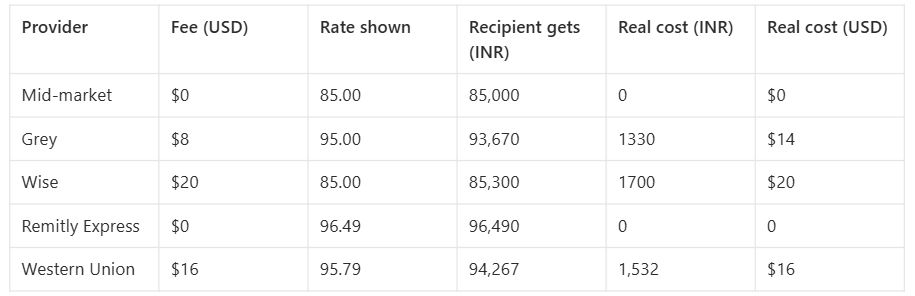

Mid-market rate at time of comparison: 1 USD = 85.00 INR. Theoretical maximum: INR 85,000.

The provider delivering the most INR is the cheapest. Period. The fee and the rate are intermediate numbers. The INR received is the final answer.

What the worked example reveals

In most comparisons on most days, Remitly and Grey deliver the most INR for amounts in the $500–$2,000 range. Wise usually comes next, while Western Union typically delivers the least due to its combined fee-plus-margin structure. Remitly’s Express option and Grey are often preferred because they balance competitive fees with stronger exchange rates.

But this ranking can shift. On days when the USD-INR rate is volatile, different providers update their rates at different speeds. A provider that updates every 30 seconds may offer a better rate than one that updates hourly, or vice versa, depending on which direction the rate moves. This is why you should always check on the day you send, rather than relying on a comparison from the previous week.

Also read: A guide for Indians getting paid by clients abroad

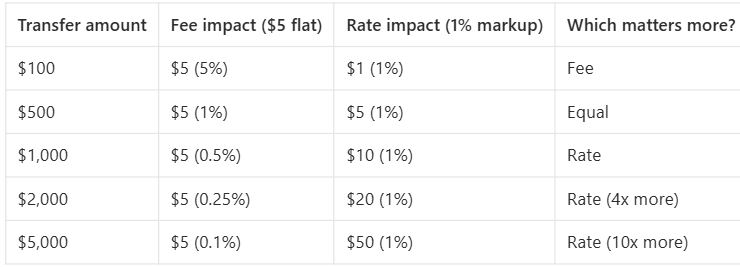

The answer depends on the amount you are sending.

Small transfers: under $200

The fee dominates. A $5 fee on a $100 transfer is 5%. A 1% rate markup on $100 is only $1. At this amount, the fee is 5x more expensive than the rate spread. For small transfers, choose the provider with the lowest fee, even if the rate is not the best.

Medium transfers: $200 to $1,000

Fee and rate are roughly equal. A $5 fee on $500 is 1%. A 1% rate markup on $500 is also $5. At this range, you need to compare total INR delivered, because neither the fee nor the rate dominates consistently.

Large transfers: $1,000 and above

The rate dominates. A $5 fee on $2,000 is 0.25%. A 1% rate markup on $2,000 is $20. At this amount, the rate spread is 4x more expensive than the fee. For large transfers, the exchange rate is far more important than the transfer fee. A zero-fee provider with a 1.5% rate markup will cost you $30 on a $2,000 transfer, while a $5-fee provider with the mid-market rate costs $5.

If you send $500 or more to India per month, the exchange rate should be your primary comparison metric, not the fee.

USD to INR rates fluctuate throughout the day based on global forex trading, economic data releases, and monetary policy decisions. On a typical day, the rate can move 0.1% to 0.3%. On a volatile day (Federal Reserve announcement, RBI policy change, global risk events), it can move 0.5% to 1%.

What this means in practice: a $1,000 transfer sent at a 0.3% better rate delivers INR 255 more. Over twelve monthly transfers, that is INR 3,060 or roughly $36. Not life-changing, but not nothing either.

Should you try to time the market?

For most people, no. Predicting short-term currency movements is notoriously difficult, and the mental cost of checking rates daily is not worth the $2-$3 per transfer you might save. The more valuable optimisation is choosing a provider with consistently competitive rates, and then sending when you need to send.

That said, there are a few practical timing tips:

Also read: How freelancers in India can invoice clients abroad easily

If you send monthly and want to minimise cost

Use the four-step method from this guide once, on the day you plan to send. Check Grey, Wise, and your current provider for the same amount. Pick the one that delivers the most INR. Repeat each month. Over a year, this discipline can save $100-$300 compared to using the same provider without checking.

If you send infrequently and want simplicity

Set up Grey or Wise once and use it each time. Both show the rate and fee before you confirm, so you always know the cost. You do not need to run a four-provider comparison for every transfer if your amounts are under $500, since the per-transfer savings from comparison shopping are small at low amounts.

If you send large amounts ($5,000+)

The exchange rate is critical. A 0.5% difference on $5,000 is $25. Check Grey, Wise, and one or two additional providers. Consider timing your transfer to avoid volatile days. For amounts over $10,000, call your bank and ask for their wire transfer rate, as some banks offer competitive rates on large amounts that beat app-based providers.

1. What is the best exchange rate for sending money to India?

The mid-market rate is the benchmark. It is the rate banks use when trading currencies with each other, and you can check it on Google or XE for free. No consumer provider gives you this rate completely free, but Wise comes closest by charging a separate visible fee with no rate markup. Grey shows a competitive rate alongside a visible fee. Compare the total INR delivered for your specific amount on each app to find the best rate on any given day.

2. Why do some apps say zero fees but my recipient gets less INR?

Zero-fee apps build their revenue into the exchange rate. If the mid-market rate is 85.00 and the app offers 83.50, the 1.50 per dollar spread is the app's margin. On a $1,000 transfer, that hidden margin costs INR 1,500, equivalent to approximately $17.65. You paid no fee, but the transfer cost more than a $5-fee provider using the mid-market rate would have charged.

3. How often do USD to INR rates change?

The USD to INR rate fluctuates continuously during forex trading hours. On a typical day, movements of 0.1% to 0.3% are common. On volatile days (Fed announcements, RBI policy, major economic data), movements of 0.5% to 1% are possible. Grey shows the live rate before each transfer so you can see the current rate before committing.

4. Should I wait for a better rate to send money to India?

For typical transfer amounts ($500-$2,000), the savings from timing are small. A 0.3% improvement on $1,000 is $3. The bigger savings come from choosing a provider with consistently competitive rates. For large transfers ($5,000+), checking rates over a few days before sending can save $15-$25. Avoid sending during major economic announcements when rates are volatile.

5. How do I know if a provider is adding a markup to the exchange rate?

Check the mid-market rate on Google or XE at the exact same time you check the provider's rate. If the provider's rate is lower than the mid-market rate, the difference is their markup. On a $1,000 transfer, a markup of 1.00 INR per dollar costs you INR 1,000 (approximately $11.76). Grey shows the rate and fee separately, making the total cost visible before you send.

6. What is the cheapest way to send money to India from the US?

Compare the total INR your recipient receives for the same USD amount across Grey, Wise, and your current provider. The one delivering the most INR is the cheapest for that specific transfer. For amounts under $200, the fee matters most. For amounts over $1,000, the exchange rate matters most. For ongoing transfers, Grey and Wise are typically the cheapest options because both show pricing transparently.

7. Is it cheaper to send a large amount or multiple small amounts?

Usually, a single large transfer is cheaper. Most providers charge a flat or semi-fixed fee per transaction. Sending $1,000 once costs one fee. Sending $250 four times costs four fees. The exchange rate is the same either way. Exception: if a provider has a minimum fee (e.g., $2 minimum), very small transfers ($50-$100) may pay a disproportionate cost per transaction.

Comparing money transfer rates to India helps you avoid hidden fees and get better value for every transfer. Grey makes this easier with its multicurrency feature, offering transparent and competitive transfer rates. You can send money seamlessly while tracking costs in real time. Sign up or download the Grey app to manage and send money internationally with ease.

.svg)

Back to top