Algeria is seeing a quiet shift in how consultants work. More professionals are now advising US clients, delivering projects that move easily across time zones and borders. The work flows smoothly, relationships grow, and invoices are paid in dollars without much friction on the client’s end.

Things tend to change when that payment needs to arrive in Algeria. Between the US bank, intermediary channels, and final conversion into dinars, the process can introduce delays, added fees, and exchange rates that reduce the original value. What starts as a clear amount in dollars can feel less certain by the time it reaches your account, especially when multiple financial systems are involved.

The goal is not just to get paid, but to receive your consulting income in a way that protects its value and gives you timely access. This article explains how to receive payments from US clients in Algeria, what affects the final amount, and how to approach the process with more clarity and control.

Also read: How Algerians get paid online despite banking restrictions

Receiving US payments in Algeria comes with several structural and operational challenges that affect both timing and the actual amount received. One of the main issues is limited access to global payment platforms, as some services restrict operations in certain regions or offer reduced functionality. This can force freelancers and consultants to rely on fewer options, increasing dependency risk.

Another major challenge is currency conversion losses. Fluctuating exchange rates and hidden fees can significantly reduce the final amount received compared to what was invoiced. Even small percentage deductions become meaningful over time. There are also processing delays and inconsistent transfer timelines, especially when payments pass through multiple intermediaries or banking networks. This unpredictability makes cash flow planning difficult.

Finally, the lack of transparency in fee structures makes it harder to predict earnings accurately. Without a clear system, professionals often struggle to understand what they will actually receive versus what was billed.

As an Algerian consultant working with US clients, it’s easy to look at the dollar amount you’re paid and assume that’s exactly what will land in your account. But in reality, the journey between invoice and payout involves multiple layers of deductions that quietly reduce the final figure.

For example, a client might send $1,000, but by the time it reaches you, the amount is already lower. There may be sending fees from the US bank, processing fees from intermediary banks, platform charges if you are using a payment service, and finally conversion fees when dollars are exchanged into dinars. Each step may seem small individually, but together they create a noticeable difference in your real earnings.

It is also important to understand that not all fees are unfair or avoidable. Many of these charges exist because banks and payment platforms are responsible for handling currency conversion, international compliance checks, fraud detection systems, and cross-border settlement infrastructure. These systems are complex and regulated, and their operational costs are reflected in transaction pricing.

Another factor often overlooked is exchange rate variation. Even if fees are low, a weaker conversion rate can significantly reduce your payout. This is why two consultants receiving the same $1,000 can end up with different final amounts depending on the platform they use and the timing of the conversion.

Understanding this structure helps you move from passive acceptance to informed decision-making. Instead of focusing only on the invoice amount, you start focusing on net income, platform efficiency, and timing. This awareness is what allows consultants to keep more of what they earn over time.

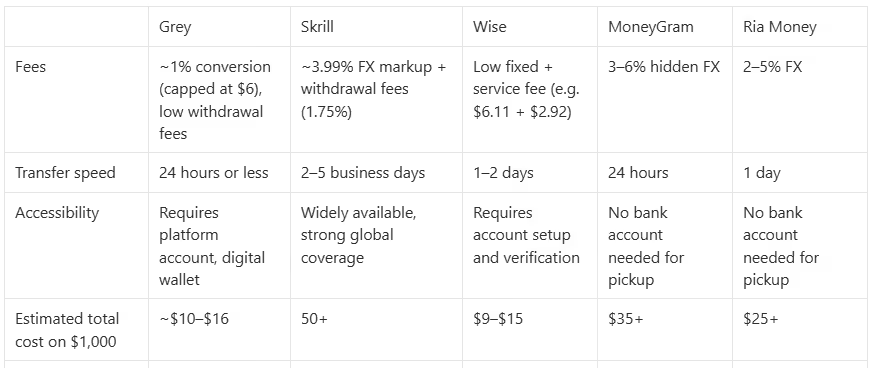

Grey

Grey is built for consultants who want to receive international payments without unnecessary complexity. You can get paid in USD, EUR, or GBP and manage everything in one place. One of its strongest advantages is transparency; fees are clearly displayed before transactions are confirmed, reducing uncertainty.

Conversion fees are typically around 1%, capped at about $6, which makes it competitive compared to traditional banking systems. Withdrawals vary depending on currency and destination, but overall costs remain relatively low compared to legacy international transfers. Most payments arrive within 24 hours, which is useful for consultants managing multiple clients or recurring projects.

Beyond speed and cost, Grey also gives flexibility in how you manage funds. Instead of being forced into immediate conversion, you can decide when to convert or withdraw based on market conditions. This gives you more control over your earnings and reduces exposure to unfavorable exchange rate movements.

Skrill

Skrill is a widely accessible payment option that allows consultants to receive money through cards, bank transfers, or digital wallets. It is relatively easy to set up and is accepted across many platforms, making it convenient for freelancers working with diverse clients.

However, its cost structure can be high. Currency conversion typically adds around 3.99% to the exchange rate, which directly reduces your earnings. On top of that, withdrawals to bank accounts often carry fees of around 1.75% or a minimum fixed charge, depending on the amount transferred.

Transfer times usually range between 2 and 5 business days, which may not be ideal for consultants who rely on faster cash flow cycles. While Skrill is reliable and secure, it tends to be more suitable for occasional payments rather than structured consulting income where small losses accumulate over time.

Wise

Wise is known for transparency and the use of real mid-market exchange rates. Unlike many traditional services, it avoids hidden markups and clearly shows all costs upfront, making it easier for consultants to understand exactly what they are receiving.

For transfers into Algeria, fees may include a fixed wire charge of around $6.11 plus a small service fee of about $2.92, depending on the transaction size. Payments usually arrive within 1–2 days, making it both fast and predictable for consulting work.

Wise is especially useful for consultants with regular US clients because it allows clearer financial tracking. Since exchange rates are more stable and transparent, it becomes easier to forecast income and manage monthly cash flow with greater confidence.

MoneyGram

MoneyGram is useful for consultants who need fast access to cash without relying on traditional banking infrastructure. Payments can be sent online or through physical agents, and recipients in Algeria can collect funds directly. This makes it highly convenient in urgent situations, especially when speed is more important than cost efficiency. However, fees are relatively high, usually ranging from $5 to $25 depending on the amount sent. In addition, exchange rate markups of around 3–6% are common.

Because of this, MoneyGram is best suited for emergency or one-off payments rather than consistent consulting income. Over time, the hidden cost of exchange rates can significantly reduce total earnings.

Ria Money Transfer

Ria Money Transfer offers fast international transfers with relatively simple access. Payments are usually completed within a day, and recipients can collect cash from local agents without needing a bank account.

Fees are generally low, starting from around $1.99 to $2.99, depending on the funding method. Card transfers are often faster, sometimes arriving within minutes, while bank transfers may take a few days to complete.

Despite its convenience, exchange rate margins still apply, which reduces the final value received. Ria is useful for quick or occasional payments but less efficient for structured consulting income where consistency and cost control matter more.

Also read: How Algerians get paid online despite banking restrictions

Receiving payments from US clients in Algeria can be smooth when the process is structured properly. Most delays are not caused by clients, but by inconsistencies or missing information in the payment chain.

Clear invoicing is essential. Your legal name, account details, and client information should match exactly across all platforms. Even minor inconsistencies can trigger compliance checks, leading to temporary holds or verification requests.

Payment descriptions also matter more than many consultants realize. Vague notes like “freelance work” or empty descriptions can slow processing. Clear labels such as “consulting services” or specific project names help financial systems classify transactions correctly.

Keeping supporting documentation ready is also important. Contracts, agreements, and email confirmations may be required for verification. Having them available reduces delays, especially for larger or recurring payments that are more likely to be reviewed.

Finally, using platforms designed for cross-border payments reduces friction significantly. Services like Grey or Wise structure transactions in a way that aligns with compliance requirements, reducing manual checks and improving processing speed.

Also read: The ultimate digital bank account for freelancers in Algeria

Receiving payments once is simple, but building a stable system is what creates long-term consistency.

Instead of treating every payment as a separate event, consultants benefit from standardising their payment process. Using one or two platforms consistently helps you understand fees, predict timelines, and reduce uncertainty.

Client communication also plays a role. Standardised invoices, consistent payment instructions, and clear descriptions reduce mistakes and ensure smoother processing on both sides.

Finally, tracking income properly is essential. Recording what you invoice, what you receive, and what is deducted helps you understand your real earnings. Over time, this gives you better pricing power and financial clarity.

1. Why do US payments to Algeria sometimes take longer than expected?

Delays usually come from compliance checks, not the client. Banks and payment platforms review transactions for security, especially cross-border ones. If details are unclear or documents are missing, payments are paused. Once information matches correctly, funds are usually released without issue, just sometimes slower than expected.

2. How can I reduce the chances of my payment being blocked?

You reduce risk by keeping your identity, invoice, and payment details consistent. Use the same name across platforms, send clear invoices, and ensure your client describes the service properly. Avoid vague transaction notes. Consistency helps systems recognise your income as legitimate and process it faster.

3. Do small payments get processed faster than large ones?

Yes, generally smaller payments move faster because they trigger fewer compliance checks. Larger payments often require extra verification, such as invoices or contracts. However, if your documentation is strong and consistent, even large payments can be processed smoothly without long delays or unnecessary questioning.

4. Is it better to use banks or digital platforms for US payments?

For Algerian consultants, digital platforms are often smoother because they are built for cross-border work. They reduce manual checks, show clearer fees, and speed up transfers. Banks are secure but slower due to stricter compliance rules. The best choice depends on your payment frequency and urgency.

For Algerian consultants working with US and global clients, reliable foreign payment solutions are essential. Grey is designed for freelancers, consultants, and remote professionals who need a simple way to receive USD, EUR, and GBP from international clients.

Algerian consultants can open foreign accounts within minutes, access cross-border payments at low, transparent fees, and withdraw funds to local accounts quickly. It also helps reduce delays, avoid hidden charges, and improve control over international earnings. Sign up on Grey or download the app to get started.

Grey charges fees on deposits, conversions, and withdrawals. Deposits via ACH, SEPA, or FPS incur a 0.8% fee (minimum $2/€2/£2, maximum $10/€10/£10). Currency conversions are charged at 1%, capped at $6. Withdrawal fees vary by currency: ₦35 for NGN, 0.5% for EUR/GBP (minimum €2/£2, maximum €10/£10), and $0.50-$0.65 for KES/UGX/TZS. Cross-border card transactions (non-USD purchases on a USD card) incur a 2% fee plus $0.50. Exchange rates are variable and include a margin over the mid-market rate. Always review fees and the rate before confirming a transaction. Visit grey.co/pricing for current rates.

.svg)

Back to top