Let’s say you are consulting for a UN agency, advising on a particular project and monitoring its execution. Your contract terms have been settled, and they will pay you in USD, EUR, or GBP. All that is left for you to do is provide your payment details, until you realise there is a problem.

Managing international payments as a consultant in Nigeria differs from freelancing, especially in how payments are structured. Consulting roles are often project-based and long-term, meaning the payment cycle can be longer, payments can be phased, and the total value can be higher. Delays are more disruptive to your cash flow, and markups on conversion rates lead to greater loss. International corporations, global NGOs, and foreign clients will opt for the easiest payment option for them, not necessarily the most cost-efficient for you.

This article explains the challenges of receiving international consulting payments, how to receive them, and how to structure your setup to avoid cash flow disruptions and unnecessary losses.

Understanding the challenges of receiving consulting payments from abroad in Nigeria will help avoid costly or inefficient payment routes..

International wire transfers often pass through several intermediary banks, each charging fees that can reduce the final amount by $20–$50 per transaction. In total, intermediary and conversion costs can reduce the payment value by 3–7%.

Most standard local banks cannot hold foreign currencies. So, your payment is converted to naira immediately and often at an unfavourable rate because many local banks charge high markups on converting USD, EUR, or GBP into Naira.

Naira is more volatile than foreign currencies. As the value of the naira fluctuates, it makes it hard to predict the exact amount you are getting, affecting financial planning and income stability

International transfers can take several business days or, in some cases, over a week to get to your local account.

Local banks frequently request extensive documentation (invoices, contracts) to justify inflows, leading to further delays.

If you are looking for practical ways to receive consultation payments in Nigeria, here are your options.

Some clients, particularly larger corporations with rigid accounts payable processes, will only pay via bank wire via SWIFT, regardless of any alternatives you offer. In those situations, a domiciliary account at a Nigerian commercial bank is the appropriate receiving mechanism.

A major drawback with this option is the cost. Your client's bank charges them between $25 and $45 to initiate the wire. The money might have to go through one or more intermediary banks, which could add $15-$60 in transit fees, depending on the number of intermediaries. Your receiving bank may charge a receiving fee or a transfer fee on top of that. Also, you are kept in the dark concerning these fees, so you typically don’t know the final amount until it arrives two to five business days later. International wire fees can reduce payments by 3–7% when all intermediary and conversion costs are combined.

SWIFT payments might be better suited for infrequent large-sum payments. This is the only way to ensure you don’t lose too much to the fees.

Also read: Alternatives to domiciliary accounts in Nigeria

If you are in a structured, ongoing retainer arrangement with a single foreign client, contractor platforms like Deel, Remote, or Ripple handle the payment infrastructure on both sides, which simplifies the process.

Your client pays the platform in their local currency. The platform handles currency conversion, contractor compliance documentation, and local payout to your Nigerian bank account in naira. You receive a fixed amount on a regular schedule without managing the conversion or transfer yourself.

Deel supports payouts to Nigerian bank accounts and handles naira conversion internally. As with traditional bank accounts, exchange rates and transaction costs may not always be transparent. But this option suits consultants in long-term arrangements with a single client better than it suits those managing multiple engagements simultaneously. It is not designed for a consultant who issues different invoices to different clients each month.

Also read: Setting up payment terms and timelines with international clients

For most Nigerian consultants working with international clients, a virtual foreign-currency account can be a more efficient way to manage international payments. Unlike traditional banks, these accounts are designed to handle foreign currencies without forced conversion, giving you better control over your income.

When you open a virtual USD account through a fintech platform, you receive a real US routing number and account number issued through the platform's licensed US banking partner. For example, ACH payments move through US domestic rails, which reduces intermediary bank involvement compared to SWIFT transfers.

The money lands in your virtual USD account, typically within one to three business days for ACH. You hold it in USD, convert when the rate is favourable, and withdraw to your Nigerian bank account.

Here are some examples to consider:

Where feasible, crypto payments offer a borderless payment option. It is nearly instant and usually low-cost. Stable coins like USDC and USDT are backed by USD, so they are not volatile. Dedicated crypto platforms like Breet and Payrite, as well as digital payment platforms like Grey and Cleva, help consultants receive stablecoins easily and convert to fiat currency within minutes or a few hours.

Understanding how international consulting payments flow can help you better manage your payments.

Traditional bank wire transfers use SWIFT and involve a chain of banks. The client initiates the transaction from their bank to yours. The sender bank sends an encrypted SWIFT message that contains the payment instructions. The money moves from the sender bank to one or more intermediary banks. Intermediary banks convert currencies with a markup on the exchange rate, charge fees, and may delay funds reaching your Nigerian bank account. Here is a summary:

Virtual USD accounts work like regular US accounts. So, these transactions look less like international transactions and more like local payments. USD transactions are processed via ACH and sent directly from the sender’s bank to your USD account, which avoids intermediary banks, their fees, delays, and forced conversions. In essence:

Once you sign up with a payment platform that supports stablecoins, get your wallet address for the specific stablecoin and share it with the client. The sender initiates the transaction from their crypto wallet using an agreed-upon standard (a payment network). This is what USDC/USDT transactions look like:

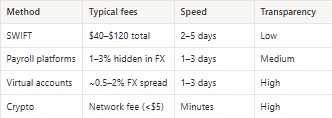

Here is a table to help you visualise the difference between each payment method.

Choosing how you receive payments is only half the equation. The terms you set determine when the money is due, and the combination of good terms and good infrastructure is what keeps your cash flow healthy. A few things you should consider when drafting your consulting contracts before any work begins:

Also read: How consultants structure international client payments

Receiving consulting payments from abroad in Nigeria is now more accessible with the right setup. You can get paid faster, reduce fees, and maintain control over your earnings.

For Nigerian consultants, Grey provides virtual USD, GBP, and EUR accounts with international banking details. Fees are clearly stated, and exchange rates are applied close to the mid-market rate, with a transparent spread on each conversion, so you know exactly what you receive.

Sign up on Grey today and download the app to manage your international consulting payments with more control and visibility.

.svg)

Back to top