For a long time, a domiciliary account was the go-to answer for Nigerians who needed to hold or receive foreign currency. If you had reasons to manage USD, GBP, or EUR, you would need to visit a Nigerian bank and complete the rigorous paperwork to open a domiciliary account at a local bank. Despite the transaction delays and restricted access to foreign currency, it seemed like the best thing since sliced bread. Dom accounts were all we had, and we had to make do with them.

Things have now changed. We have better options for managing foreign currency and many Nigerians are looking away from dom accounts. This article explores the alternatives, what each offers, and helps you pick the right one for how you earn and spend.

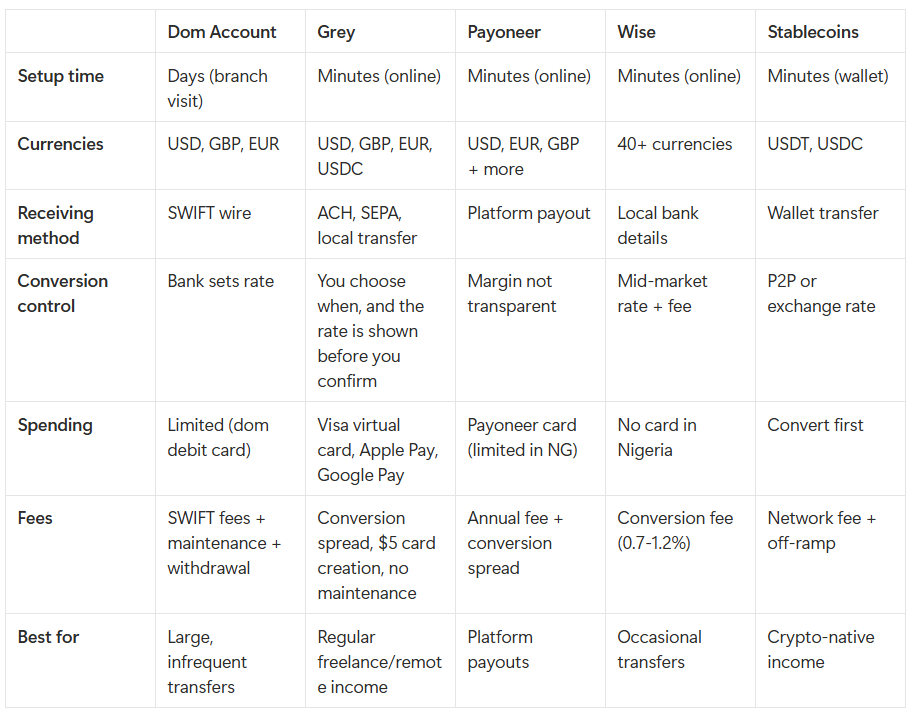

A domiciliary account is a foreign currency account offered by Nigerian commercial banks. It lets you hold USD, GBP, or EUR without immediate conversion to naira, and receive international transfers directly into a local account.

On paper, that sounds like a reasonable way to manage international payments. In practice, the experience rarely matches the description.

Opening a dom account typically requires a visit to a physical branch, a referee who already holds an account at the bank, a utility bill, a passport photograph, and, depending on the bank, an opening deposit of $100 to $200. The process can take days or longer. If you need to start receiving international payments urgently, going the dom account route means you are standing on a long thing.

Then there are the costs. SWIFT transfers to a domiciliary account incur charges on both the sending and receiving ends. The sender's bank charges a fee, intermediary banks take their cut ($15 to $50 is common), and your own bank charges a receiving fee on top. By the time the money settles, you could be looking at $30 to $70 less than what was sent, with no clear line-item breakdown of why. Some banks also impose monthly maintenance fees, withdrawal limits (both cash and transfers), and minimum balance requirements, which add friction to every interaction.

Despite the downsides, dom accounts still make sense for certain situations. If you are receiving large, infrequent wire transfers, or you want to hold a significant USD balance long-term under the regulation and deposit protection of a licensed Nigerian bank, a dom account serves that purpose. But for freelancers, remote workers, and entrepreneurs managing regular international income, the costs and friction add up quickly. That is where the alternatives come in.

Also read: Managing foreign currency earnings as a remote worker in Nigeria

Here are the real options, with enough detail on each to make a decision.

This is where most Nigerians who have moved away from dom accounts have landed, and the reasons are straightforward.

Platforms like Grey give you real USD, EUR, and GBP account details, including routing numbers, account numbers, and IBANs. These work the same way as foreign bank accounts from the sender's perspective. When your client in New York pays you via ACH using your Grey USD account details, it looks like a standard domestic transfer on their end. There is no SWIFT involved, which means no intermediary bank fees eat into your payment. The funds arrive in your Grey wallet, typically the same day for ACH transfers, and you can see the balance in the app immediately.

From there, you have options. You can hold the dollars in your wallet and convert to naira when the rate works for you, rather than being forced to convert at your bank's rate on the day the transfer arrives. You can spend the dollars directly using a Grey virtual card on subscriptions, software, advertising, or anything else that charges in USD. The card works everywhere Visa is accepted and supports Apple Pay and Google Pay, so you can tap to pay at physical stores in supported regions. Or you can withdraw to your Nigerian bank account when you need naira.

Virtual foreign currency accounts open in minutes, completely online. There is no branch visit, no referee, and no minimum deposit. You see the exchange rate before you confirm a conversion, so you know exactly what you are paying. This is the biggest contrast with dom accounts, where SWIFT fees and conversion costs are often opaque until after the transaction has settled.

Grey is the platform on which this article is published, so take that into account. Other platforms in this category include Geegpay (popular with freelancers, offers USD/GBP/EUR wallets and a virtual dollar card), Eversend (multi-currency wallets across several African countries), and Cleva (US-based USD account with FinCEN registration). Each has a slightly different fee structure, supported currencies, and feature set. Compare them based on the currencies you need, the exchange rate spread, and how quickly you can access your funds.

Best for: Freelancers, remote workers, consultants, and anyone receiving regular international payments from clients or employers. This is the most direct replacement for a dom account for day-to-day use.

Also read: How Nigerian freelancers scale income beyond one platform

Wise (formerly TransferWise) is one of the most well-known names in international money movement, and many Nigerians use it. You can open a Wise account from Nigeria and get USD, GBP, and EUR account details for receiving payments. Wise's biggest selling point is that it uses the mid-market exchange rate with a transparent fee on top, rather than hiding the cost in the rate spread. For outbound transfers, this is genuinely cheaper than most alternatives.

However, Wise has significant limitations for Nigerian residents that are worth understanding before you rely on it as your primary account.

No physical card in Nigeria. The Wise multi-currency card is not available for Nigerian residents, which limits your spending options to transfers and online payments.

Service disruptions. Wise has periodically adjusted its operations in Nigeria. In 2022, it suspended USD transfers to Nigeria due to infrastructure constraints. These disruptions can be disruptive if Wise is your only receiving option.

Strict anti-crypto policy. Wise prohibits transactions related to cryptocurrency. If the platform detects a transfer to or from a crypto exchange, it may permanently close your account. For Nigerian professionals who also deal in stablecoins, this is a real risk.

Not a bank. Wise is an Electronic Money Institution, not a bank. Your funds are held in safeguarding accounts, not in a bank account in your name. This is a technical distinction, but it matters if you are considering where to hold a large balance in the long term.

Best for: One-off or occasional international transfers where you want the best exchange rate. Less suitable as a primary account for Nigerian residents who need a card, regular access, or crypto flexibility.

Payoneer is an option many Nigerian freelancers encounter first, largely because of its strong integration with major international platforms. Upwork, Fiverr, Amazon, and dozens of other marketplaces offer Payoneer as a payout option. If your income comes primarily through those platforms, Payoneer remains a viable option.

However, Payoneer's conversion rates are not as transparent as those of newer platforms. There are also annual fees for accounts that do not meet certain activity thresholds, relatively high transaction charges compared to fintech alternatives, and an occasionally frustrating customer support experience. The NGN withdrawal rate is not always the best either; you may find better naira conversion rates on platforms like Grey or Geegpay.

Payoneer works best when your income flows through freelancing platforms that have native Payoneer integration. For direct client payments where you control the payment method, a virtual foreign currency account is typically a better option.

Best for: Freelancers receiving payouts from Upwork, Fiverr, Amazon, and other marketplaces that integrate Payoneer natively.

Also read: Top PayPal and Payoneer alternatives for African freelancers

Despite the evolving regulatory landscape around crypto in Nigeria, stablecoins remain a practical option for professionals who know how to use them. Some Nigerian freelancers and entrepreneurs receive payments in USDT or USDC because they retain their dollar value, transactions settle in minutes, and fees are low.

The challenge is not in holding stablecoins. It is in the off-ramp: converting USDC or USDT back to naira. Peer-to-peer conversions are popular but carry counterparty risk if the buyer is not trustworthy. Exchange platforms offer more structure but may have their own fees and verification requirements. Some fintech platforms, including Grey, support USDC alongside their multi-currency offering, which bridges the gap between the crypto and traditional banking worlds.

One important note for 2026: under the new Nigeria Tax Act, stablecoin payments are treated as foreign income. If you receive $1,000 in USDC on a given date, that income must be converted to naira at the CBN exchange rate on the date of receipt for tax purposes. The same self-declaration and filing obligations that apply to USD bank transfers apply to crypto income. This does not make stablecoins impractical, but it means you need to track your receipts the same way you would track any other foreign income.

Best for: Crypto-native professionals, developers in the Web3 space, and anyone whose clients or platforms pay in stablecoins. Not a replacement for a bank account or virtual foreign account for most people, but a useful complement.

Here is a side-by-side comparison of the key factors that matter when choosing how to manage foreign currency in Nigeria.

You earn regularly from international clients or an employer. A virtual foreign currency account is your best option. You get foreign bank details to share with clients, control over when you convert, and a card to spend directly in USD. This replaces a dom account for most day-to-day use cases.

Your income comes through Upwork, Fiverr, or Amazon. Start with Payoneer since these platforms integrate it natively. If you find the conversion rates eating into your earnings, consider adding a Grey or similar account and routing future direct client payments there instead.

You need to send a one-off international transfer and want the best rate. Wise is hard to beat on exchange rates for single transactions. Just be aware of its limitations as a full-time financial tool for Nigerian residents.

You receive large, infrequent transfers and want to hold USD for the long term. A dom account at a reputable Nigerian bank still works for this. The setup friction is a one-time cost, and the banking regulation provides a level of institutional protection that fintech platforms do not.

You are paid in crypto or stablecoins. Hold your stablecoins and use a platform that supports USDC conversion to naira when you need to spend locally. Track your receipts for tax purposes under the 2026 NRS rules.

Most Nigerians managing regular international income end up using a combination of methods. A virtual foreign account for the majority of their income, Payoneer for platform payouts, and occasionally a dom account or Wise for specific transactions. The key is to stop defaulting to the dom account for everything, because for regular use, the alternatives are faster, cheaper, and more flexible.

Grey gives you USD, EUR, GBP, and USDC account details to receive international payments, a virtual Visa card with Apple Pay and Google Pay support for spending, a built-in invoicing tool for billing clients, and naira withdrawals to your Nigerian bank account. Sign up at grey.co or download the app to get started.

Note: Exchange rates on Grey are variable and include a margin over the mid-market rate. Always review the rate before confirming a conversion.

For specific use cases, yes. If you receive large wire transfers infrequently, want to hold a significant USD balance under banking regulation, or need the institutional credibility of a commercial bank account, a dom account still serves those purposes. For regular freelance income and everyday USD spending, virtual foreign accounts are more practical.

Yes. Virtual foreign currency accounts from platforms like Grey, Geegpay, and Cleva give you USD account details that work as US bank accounts from the sender's perspective. Your client pays via ACH or wire, and the funds are deposited into your wallet without ever touching a Nigerian bank.

Virtual foreign currency accounts that support ACH transfers are typically the cheapest because they avoid SWIFT intermediary fees entirely. The main cost is the exchange rate spread when you convert to naira, which varies by provider (typically 1% to 3%).

They serve different needs. Wise offers the mid-market exchange rate, which is excellent for occasional transfers, but it has no card in Nigeria and has periodically disrupted its services in Nigeria. Grey offers a virtual card, Apple Pay/Google Pay, USDC support, and an invoicing tool, making it more practical for Nigerian residents managing regular international income. Many freelancers use both.

The regulatory landscape around crypto in Nigeria is evolving. Holding stablecoins is not illegal, and many professionals use them for international payments. Under the 2026 Nigeria Tax Act, stablecoin income is treated as foreign income and must be declared. The main risk is in the off-ramp: converting to naira through unregulated channels can expose you to fraud or compliance issues.

Not necessarily. A virtual foreign currency account with SWIFT or wire receiving capability can also receive wire transfers. However, some senders (particularly corporate treasury departments) may prefer to send to a traditional bank account. Check with your payment source whether they accept fintech account details.

Ready to move beyond the dom account? Sign up at grey.co and get your USD, EUR, and GBP account details in minutes.

.svg)

Back to top