As more Nigerians plug into the global digital economy, getting paid from international clients has become a daily reality for freelancers, remote workers, and online business owners. Whether it’s dollars from clients in the US, euros from Europe, or payments from global platforms, the question is no longer how to earn, but how to receive money efficiently in Nigeria without losing too much to fees and poor exchange rates.

Platforms like Grey, Geegpay, Payoneer, and Wise have emerged as popular solutions for receiving international payments, but they don’t all work the same way. Each comes with its own fee structure, currency conversion model, withdrawal process, and user experience, which can significantly impact how much you actually take home at the end of the day.

This comparison breaks down Grey vs Geegpay vs Payoneer vs Wise in Nigeria, helping you understand the strengths, limitations, and cost differences so you can choose the platform that best fits your income style and maximise your global earnings with ease.

Read also: Receiving dollar payments in Nigeria: Best platforms and what to avoid

Grey is basically your shortcut to having a foreign bank account without leaving Nigeria. Once you sign up, you get US, UK, or EU account details in your name. You can use these to receive payments from Shopify or any international platform like a regular business abroad. The money comes in as dollars, pounds, or euros, and you can hold it there or convert when rates make sense. You can also create a virtual dollar card, so you can spend online without stress. It’s simple, clean, and built for this exact problem, especially for freelancers managing multiple international clients regularly.

Raenest (formerly Geegpay) works in a similar way but is more tailored to freelancers and remote workers. You get foreign account details to receive payments in USD, GBP, or EUR from clients or platforms. Once the money enters, you can keep it in that currency or convert to naira when needed. It also gives you virtual cards for online payments. The main idea is to help you operate globally while still based in Nigeria, without the stress of opening a real foreign bank account, while also supporting smoother payout tracking and flexible financial management

Payoneer is one of the oldest and most widely accepted platforms for receiving international payments in Nigeria. It gives you foreign receiving accounts that connect directly to platforms like Upwork or Fiverr. Once you get paid, the money sits in your Payoneer account in dollars or other currencies. From there, you can withdraw straight to your Nigerian bank account in naira. It’s reliable and trusted globally, but sometimes the fees and exchange rates are not the best compared to newer options.

Wise is slightly different from the others. It is mainly built for sending and receiving money across countries at competitive exchange rates. If someone is paying you from abroad, Wise can deliver the money directly into your Nigerian bank account in naira, often very quickly. It uses the mid-market rate, so you avoid the usual hidden charges banks include. While it may not always give you full foreign account access in Nigeria, it is very useful for fast, transparent transfers without surprises.

Read also: How to avoid high fees when receiving international payments

In Nigeria, choosing a payment platform is not just about what looks easy at the start but about what you actually keep after every transaction. Many people only pay attention to how quickly they can receive money, but the real difference shows up in the fees and hidden costs that come after.

Some platforms charge small amounts that seem harmless at first, but once you start receiving regular payments, those deductions quietly grow into a noticeable loss. Withdrawal fees, conversion charges, and processing costs all stack up, especially when you are earning in foreign currencies like dollars or pounds.

Over time, even a 1–2% difference in fees can shape your financial stability as a freelancer. When you work with international clients, your income depends not only on how much you earn but how efficiently you can move and convert it. Understanding fee structures helps you plan better, price your services correctly, and avoid losing money silently through repeated transactions each month. This becomes crucial for consistent income growth overall.

Exchange rates are another area people often overlook. One platform might give you a fair rate close to the real market value, while another widens the gap and takes more during conversion. Over time, that difference can reduce your income significantly, even if your sales remain the same.

There is also the issue of access and timing. Some services release your funds quickly and at a lower cost, while others slow things down or add extra steps before you can touch your money. Comparing fees and structures helps you avoid unnecessary stress and choose platforms that protect your earnings. It is really about making sure your effort translates into real value at the end.

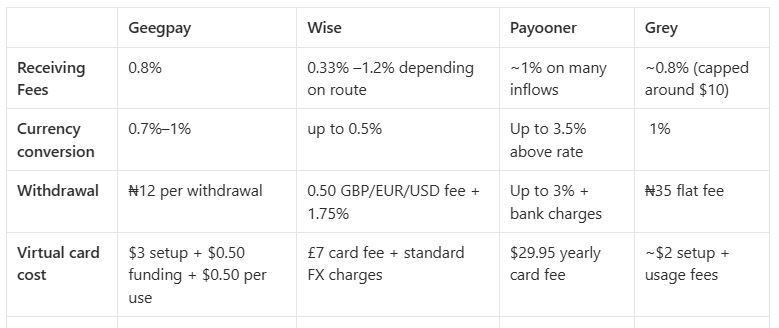

With Geegpay, the first thing you notice is how each inflow quietly carries a fee. USD comes in with about 0.8% taken (minimum $1.5, capped at $12), while GBP and EUR sit slightly lower at 0.7% with their own minimum charges that affect smaller payments more. You may not feel it on one transaction, but it becomes clear when payments start coming in regularly. Even the virtual dollar card adds extra layers, $3 to create, $0.50 to fund, and $0.50 every time you swipe.

Withdrawals into your Nigerian account are only ₦12, but they still count per transaction. It is a system that feels smooth, but teaches you to pay attention to every small deduction over time.

Wise feels different because everything is upfront and clear before anything moves. A transfer from the UK costs around £6.14, while transfers to Europe can go up to about €15.51, depending on the amount and route. Fees generally range between 0.33% and 1.2%, depending on the currency pair you are dealing with. Even the card costs about £7 to order. It feels fair because nothing is hidden, and you always know what is leaving your account. But once you start using it frequently for small or repeated transfers, the costs quietly build up.

Payoneer is one of those platforms that feels reliable because it connects you easily to global marketplaces like Upwork and Fiverr. Getting paid is usually simple, but the real costs appear when you move money around. You pay about $29.95 yearly for the card, up to 3% when withdrawing to your local bank, and up to 3.5% when converting currencies. Even internal transfers can take around 0.5% to 1%.

It works well for access, especially when you just want to receive funds without stress, but over time you start noticing how much is lost during withdrawal and conversion, especially when you rely on it as your main payout method.

Grey feels more balanced when you look closely at how the fees are structured. You pay 1% when converting currency, 0.8% when receiving foreign payments (capped at $10), and a flat ₦35 when withdrawing to your Nigerian account. The virtual card also has a $2 setup fee and about 2% plus $0.50 when used on non-USD transactions. It is not fee-free, but what makes it easier to manage is predictability. You always know what will be deducted, which helps when you are receiving regular Shopify or freelance income.

When you start looking closely at these platforms, the real difference comes down to how fees are applied and what they mean for your earnings over time.

For freelancers and remote workers, the “best” platform is rarely the one with a single low fee, it is the one with the most balanced overall structure. Some services reduce receiving fees but make up for it with wider exchange rate margins, while others offer better conversion rates but slightly higher withdrawal costs. The key is understanding your income pattern: how often you get paid, the average transaction size, and the currency you receive most often. This helps you identify which platform actually preserves more of your money in real terms.

Receiving fees may seem small, but they affect every inflow, especially if you are getting paid frequently. A 0.7%–0.8% charge on each transaction might not feel significant at first, but over multiple payments, it reduces your total income in a way that is easy to overlook.

Currency conversion is often where the biggest impact sits. Some platforms charge up to 3.5% or build their margin into the exchange rate. That difference directly affects how much naira you receive, even when your earnings in dollars or pounds stay the same.

Withdrawal fees also matter more than they seem. Fixed charges like ₦12 or ₦35 are manageable, but percentage-based withdrawals of up to 3% can take a larger share, particularly on higher amounts.

Understanding how these fees interact helps you make more informed decisions. It ensures you are not just receiving payments, but actually keeping more of what you earn in a consistent and predictable way.

The difference usually comes from FX spreads, conversion timing, and intermediary charges within the payment chain. Even when rates look stable, small percentage deductions at each stage reduce your final payout, especially in multi-currency transactions involving cross-border settlements.

Delays often occur due to compliance verification, banking holidays across regions, or intermediary bank routing. Payments involving multiple currencies or countries typically take longer because each financial layer must clear and reconcile the transaction before release.

Exchange rates fluctuate constantly, so the moment your payment is converted can significantly impact your final payout. If conversion happens during a weaker rate window, you receive less local currency even if the original dollar amount remains unchanged.

Differences come from FX conversion models and fee structures. Grey and Geegpay often apply tighter spreads, Wise uses mid-market rates with transparent fees, while Payoneer embeds higher FX margins, meaning the same $100 can convert to different naira amounts across platforms.

You should consider total cost (FX + fees), settlement speed, transparency of rates, and withdrawal ease. Wise prioritises transparency, Grey focus on competitive FX, speed and security, while Payoneer offers broad acceptance but often at a higher overall cost.

For freelancers in Nigeria, every naira counts, and the platform you choose directly affects what you take home. Once you start comparing fees, speed, and how predictable each option is, the differences become clear over time.

Grey stands out because it keeps things simple and consistent. You are typically charged about 0.8% when receiving foreign payments (capped at $10) and 1% for currency conversion, which helps you plan better without unexpected deductions. The fees are not just lower, they are easier to understand.

Sign up on Grey or download the app to start receiving your payments more smoothly and with better control.

Grey charges fees on deposits, conversions, and withdrawals. Deposits via ACH, SEPA, or FPS incur a 0.8% fee (minimum $2/€2/£2, maximum $10/€10/£10). Currency conversions are charged at 1%, capped at $6. Withdrawal fees vary by currency: ₦35 for NGN, 0.5% for EUR/GBP (minimum €2/£2, maximum €10/£10), and $0.50-$0.65 for KES/UGX/TZS. Cross-border card transactions (non-USD purchases on a USD card) incur a 2% fee plus $0.50. Exchange rates are variable and include a margin over the mid-market rate. Always review fees and the rate before confirming a transaction. Visit grey.co/pricing for current rates.

.svg)

Back to top