Every eke market day, a new payment platform joins the market, promising Nigerians an efficient way to manage USD. While the healthy competition has helped the Nigerian payment sector grow over the last couple of years, it has also left Nigerians with many questions when choosing a payment platform. Doing 'eeny, meeny, miny, moe' with how you manage your money is never a good idea. It is imperative that you weigh your options, the perks and the drawbacks before choosing.

This article breaks down the best dollar account apps in Nigeria right now, what each does well, where each falls short, and which user type each is best suited for.

Before getting into the individual platforms, here are the factors that actually matter when comparing dollar account apps.

Account details. The goal is to have real US banking details, including a routing number and account number, so clients and platforms can pay into the account directly. Not all apps provide this. Some only offer wallet-to-wallet transfers, which limits who can pay you.

Currencies supported. Some apps are USD-only. If you work with UK or European clients, you may need GBP or EUR accounts as well. Multi-currency support in a single app means fewer platforms to manage.

Fees and conversion rates. This is where most of the differences lie. Consider receiving fees, conversion spreads, card creation fees, monthly maintenance charges, and withdrawal costs. Some platforms have low headline fees but add markups to the exchange rate. Others are transparent upfront but charge for services you might not expect.

Spending options. A virtual dollar card lets you spend your USD directly on subscriptions, software, and online purchases without converting to naira first. Check whether the app offers a card, what it costs, and whether it supports Apple Pay or Google Pay for contactless payments.

With those criteria in mind, here is how the main options compare.

Also read: How Nigerian freelancers get international clients

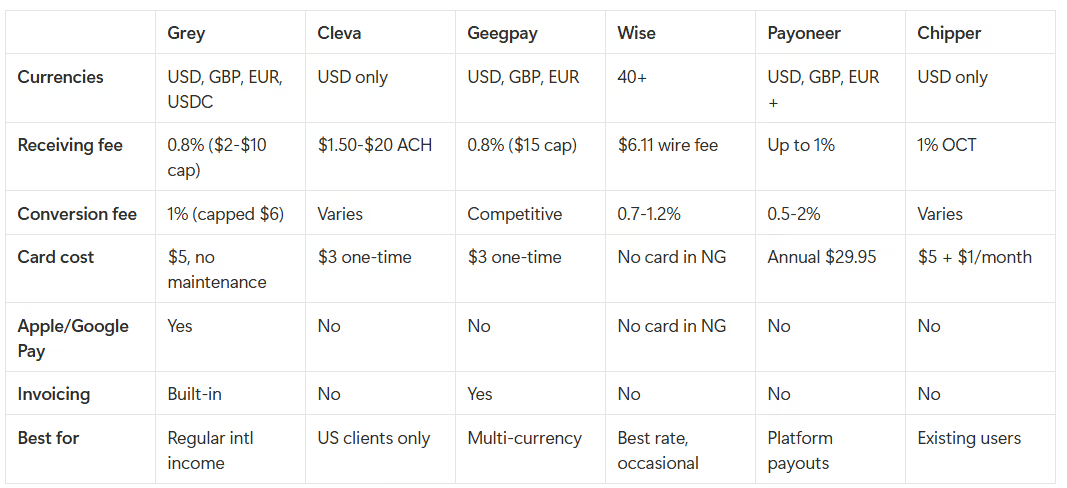

Grey is one of the most popular apps for Nigerians who regularly receive international payments. It provides multi-currency accounts in USD, GBP, and EUR, with real US banking details (routing number and account number) that you can share with clients or add to freelancing platforms. Grey also supports USDC, which bridges the gap for users who receive payments in stablecoins.

The platform is designed for remote workers and digital professionals who need to manage foreign income without relying on traditional banks. Account setup takes a few minutes with a valid ID, and you get your USD account details immediately. Grey's virtual Visa card costs $5 to create, has no monthly maintenance fee, and supports Apple Pay and Google Pay in supported regions. The card works everywhere Visa is accepted, so you can spend your USD directly on subscriptions, software, and advertising without converting to naira first.

Grey also includes a built-in invoicing tool, which is useful if you bill international clients directly rather than through a platform.

Fees: 0.8% for payments received via ACH, SEPA, and FPS, with a minimum of $2 and a cap of $10. GBP deposits via BACS cost a flat £15, and CHAPS costs £25. Currency conversion is 1%, capped at $6 per transaction. Cross-border card transactions (using your USD card on non-USD websites) incur a 2% + $0.50 fee, which is a standard card network charge. N35 for naira withdrawals. No account maintenance fee. Virtual card creation is $5.

Limitations: The conversion spread, while transparent, is not the lowest in the market for every currency pair. Grey works best when you receive payments regularly and use the card for USD spending. If your only need is a one-off transfer with the absolute lowest conversion cost, Wise may edge it out on rate.

Best for: Freelancers, remote workers, and entrepreneurs who receive regular international payments and want to receive, convert, spend, and invoice in one platform.

Cleva is gaining popularity among Nigerian freelancers for its speed and reliability. The platform provides real US account details and supports USD transactions via ACH and wire transfers. Withdrawals to Nigerian bank accounts are typically fast, and the platform has an active, growing user base.

Cleva currently supports only USD, which is a significant limitation if any of your clients are based in the UK or Europe. If a UK client pays you in GBP, you either need a second platform for that currency or you take a conversion hit somewhere in the chain. Cleva offers a virtual USD card with a small creation fee, and the capped withdrawal fees make it cost-effective for higher-value transactions.

Fees: ACH transfers have a minimum fee of $1.50 and a maximum of $20. Card creation is a one-time $3 fee (includes $1 initial deposit). 1% fee to fund the card.

Limitations: USD only. No GBP or EUR support. No built-in invoicing.

Best for: Freelancers who work exclusively with US clients and only need USD.

You may also like: Managing foreign currency earnings as a remote worker in Nigeria

Geegpay (now rebranded as Raenest) is a financial platform designed for freelancers, remote workers, and digital nomads in Africa. It provides multi-currency accounts in USD, GBP, and EUR with real bank details. Users can receive payments from platforms like Upwork, Fiverr, and Deel. The onboarding process is straightforward, the app has a responsive interface, and support is generally well-reviewed. Geegpay is a solid all-rounder and one of the more competitive options in terms of rates.

Fees: 0.8% for USD deposits, capped at $15. Virtual card creation is $3. $0.50 per card transaction. 2% international transaction fee for non-USD transactions. No monthly maintenance fees.

Limitations: The $0.50 per card transaction fee adds up if you use the card frequently for small purchases. The 2% non-USD transaction fee is notable if you spend in currencies other than dollars.

Best for: African freelancers and remote workers who want a multi-currency account with competitive receiving fees and a clean app experience.

Wise is one of the most recognised names in international money movement globally. Nigerian residents can open a Wise account and get USD, GBP, and EUR account details for receiving payments. Wise's biggest advantage is that it uses the mid-market exchange rate and charges a transparent, low conversion fee of typically 0.7% to 1.2%. For outbound transfers and one-off conversions, this is genuinely cheaper than most alternatives.

However, Wise has significant limitations for Nigerians. The Wise multi-currency card is not available in Nigeria. The platform has periodically disrupted its services in Nigeria (suspended USD transfers to Nigeria in 2022). And Wise has a strict anti-crypto policy; if the platform detects transactions linked to crypto exchanges, it may close your account. Wise is also an Electronic Money Institution, not a bank, which means your funds are held in safeguarding accounts rather than in a bank account in your name.

Fees: Conversion fee of 0.7% to 1.2% depending on the currency pair. Mid-market exchange rate with no markup. Receiving USD or CAD wire transfers costs a fixed $6.11 or $10 CAD, respectively. No monthly fees.

Limitations: No card in Nigeria. Periodic service disruptions. Strict anti-crypto policy. Not ideal as a primary account for Nigerian residents.

Best for: Occasional international transfers where you want the absolute best exchange rate. Less suitable as a primary dollar account for regular use in Nigeria.

If you have been around for some time, you might be familiar with Payoneer. It is a household name in freelancing, thanks to its seamless integration with platforms like Upwork, Fiverr, and Amazon. If your income primarily comes from those platforms, Payoneer is often the default payout option and requires the least additional setup.

Unfortunately, the exchange rates have hidden margins that make them less favourable than newer platforms. The fees are spread across multiple touchpoints, and it is only a matter of time before they add up and significantly erode your earnings.

Fees: Up to 1% for receiving USD. Up to 3% for credit card payments. $3.15 for ATM withdrawals. Annual fee of $29.95 if you receive less than $6,000 in 12 months. 0.5% to 2% for currency conversion. Up to 2.75% for certain bank withdrawals.

Limitations: High cumulative fees. Annual inactivity charge. Conversion margins not transparent. Customer support can be slow.

Best for: Freelancers receiving payouts from Upwork, Fiverr, Amazon, and similar marketplaces where Payoneer is natively integrated.

Also read: Best Payoneer and PayPal alternatives for freelancers in Africa

Chipper Cash is best known for peer-to-peer transfers across Africa, but it also offers a virtual dollar card. Nigerians who already use Chipper for local transfers can use the dollar account feature without opening a separate app. It is the most convenient option if you are already in the Chipper ecosystem.

Fees: $5 to create a USD card. $1 monthly maintenance fee per card. $0.90 flat fee on USD card transactions. 1% fee for original credit transactions (receiving money from external sources).

Limitations: The $1 monthly maintenance fee is charged whether you use the card or not. The $0.90 per-transaction flat fee makes it expensive for frequent small purchases. Limited to USD.

Best for: Existing Chipper Cash users who want a simple dollar card for occasional international purchases without switching apps.

You earn regularly from international clients in multiple currencies. Grey or Geegpay. Both support USD, GBP, and EUR with competitive fees. Grey adds USDC support, Apple Pay/Google Pay, and built-in invoicing. Geegpay has a slight edge on the receiving fee cap ($15 vs $10 on Grey, but Grey's minimum is lower).

You work exclusively with US clients and only need USD. Cleva. USD-only, but the fee structure is straightforward, and the capped ACH fees are cost-effective for larger transactions.

Your income comes through Upwork, Fiverr, or Amazon. Start with Payoneer for the native integration. But if the fees start eating into your earnings, add Grey or Geegpay for direct client payments and route new income there.

You need the absolute lowest conversion cost per transaction. Wise. The mid-market rate is hard to beat. But without a card in Nigeria or reliable full-service access, it is a transfer tool, not a primary account.

You already use Chipper Cash and just want a dollar card. Chipper's USD card works, but the $1 monthly fee and $0.90 per-transaction fee make it expensive for regular use. Worth it for convenience if you are already in the ecosystem, not worth switching to.

Most Nigerian freelancers managing high international income end up using two platforms: one primary account for receiving and spending (Grey, Geegpay, or Cleva), and Payoneer for marketplace payouts. That combination covers most situations.

Grey gives you USD, GBP, EUR, and USDC accounts, a Visa virtual card with Apple Pay and Google Pay, built-in invoicing, and naira withdrawals, all in one app. Sign up at grey.co or download the app to get your account details in minutes.

Note: Exchange rates on Grey are variable and include a margin over the mid-market rate. Fees listed are accurate as of the date of publication and may change. Always check the platform's current pricing before committing.

It depends on your usage pattern. For receiving payments, Grey and Geegpay both charge 0.8% with different caps. Cleva's flat ACH fee ($1.50 to $20) is cheaper for large single transactions. For conversion, Wise offers the lowest rate (0.7% to 1.2% at mid-market) but has no card in Nigeria. For overall value, including a card and multi-currency support, Grey and Geegpay are the most cost-effective for regular use.

Grey supports USD, GBP, EUR, and USDC. Cleva supports USD only. If you only work with US clients and only need dollars, Cleva's simpler fee structure may work. If you need multiple currencies, a card with Apple Pay support, or an invoicing tool, Grey covers more ground.

For marketplace payouts (Upwork, Fiverr, Amazon), yes, because the native integration is hard to replace. For direct client payments, newer platforms like Grey and Geegpay offer better rates and more features. Many freelancers keep Payoneer for platform payouts and use a separate app for everything else.

For regular freelance income and online USD spending, a dollar account app is faster, cheaper, and more flexible. A domiciliary account at a Nigerian bank makes more sense for large, infrequent wire transfers or long-term USD storage under banking regulation. Many people use both.

Most of these platforms are designed for individuals and sole proprietors. If you run a registered business with multiple team members, check whether the platform offers a business tier. Grey offers Grey Business for companies that need multi-user access and business-level features.

Ready to compare for yourself? Sign up at grey.co and get your USD account details in minutes.

.svg)

Back to top