Sending US dollars (USD) internationally to Egypt can feel unnecessarily complicated. You have to factor in fees, banking systems, processing times and, most importantly, choose the right transfer method.

ACH and SWIFT are the two most commonly used systems for sending money internationally, but they work differently. In this article, we’ll explain how each method works, including the costs, speed, and volume capacity, and help you decide which makes better sense for sending USD to Egypt.

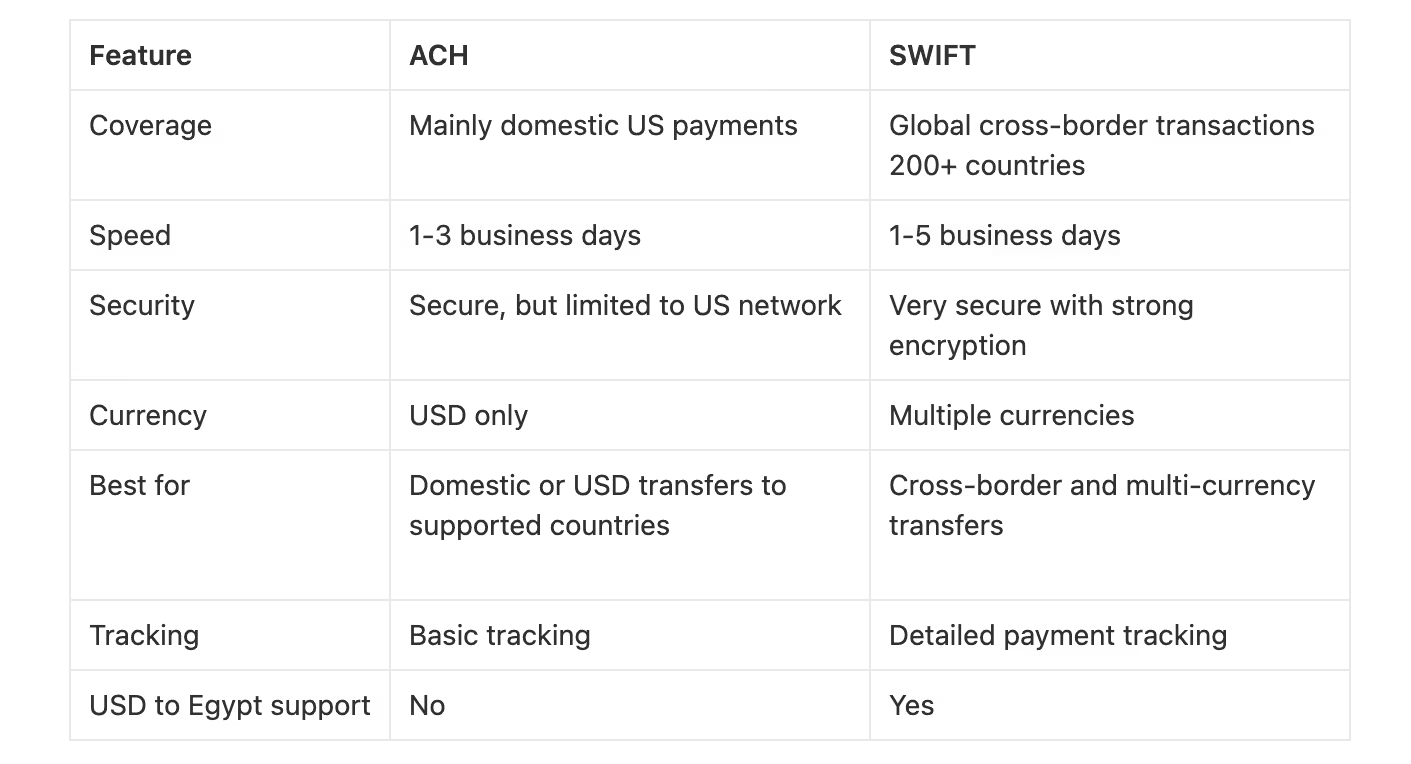

Automated Clearing House (ACH) is a money transfer system used to move money between US-based bank accounts. It’s typically used for salary payments, tax refunds, and bill payments.

ACH is known for being cost-effective, especially compared to wire transfers. Processing times are typically between one and three business days.

Advantages of ACH transfers

Cost-effective: ACH transfers are typically cheaper than wire transfers, making them a great option for routine payments.

sending and receiving money domestically easVolume: ACH supports high-volume transactions, making it a great option for businesses.

Supports recurring payments: It’s perfect for scheduled payments like subscriptions or loan repayments.

Widely accepted: Most US banks and businesses support ACH payments, making it easy to send and receive money domestically.

Disadvantages of ACH transfers

Limited to specific countries: Being a US-based system, ACH isn’t designed for direct international transfers. Banks often try to rely on intermediary services to receive ACH payments, making the process more complex and unsuitable for sending USD to Egypt.

Slow international transfers: ACH transfers are fast within the US but can take longer for cross-border payments.

Transfer limits: Many ACH providers set daily or monthly limits, which can be restrictive for users.

What is SWIFT?

SWIFT (Society for Worldwide Interbank Financial Telecommunications) is a standardised messaging system banks use to send cross-border payments. SWIFT connects over 11,000 institutions in more than 200 countries.

Many prefer SWIFT for international transfers because of its global reach, support for multiple currencies, strong encryption, and the ability to track payments.

Advantages of SWIFT transfers

Global coverage: SWIFT is supported in over 200 countries, making it one of the most widely used systems for international payments.

Supports multiple currencies: It allows you to send money in various currencies, making it useful for international trade and remittances.

Secure and reliable: SWIFT uses advanced encryption and follows global compliance standards, keeping your payment data secure.

Payment tracking: You can track the status of your transfer through a unique transaction reference, offering more transparency.

Used by trusted institutions: Major banks and financial services around the world rely on SWIFT for cross-border payments.

Good for large transfers: Ideal for sending large sums internationally, especially for business or investment purposes.

Disadvantages of SWIFT transfers

Hidden fees: SWIFT’s payment fees are often not clear from the outset. As a result, you’d typically not know how much your recipient will receive after the deductions.

Slower processing times: Transfers can take one to five business days depending on the banks and countries involved.

High fees: SWIFT transfers often come with higher costs, including intermediary and receiving bank charges.

.svg)