A freelancer has just finished a project for a client in Paris, and a message comes in: payment sent in euros. For a moment, it feels like everything has worked.

By the next morning, a different question takes over. How does that €300 or €500 actually reach Algeria without being reduced from what was originally sent?

That question is not unusual. It reflects a wider reality for many people working remotely in Algeria today, especially those earning from Europe, where getting paid is straightforward, but receiving the money locally is not always as smooth.

This article explains the best ways to receive euros in Algeria, what affects the amount you keep, and how to avoid unnecessary losses during the process.

Receiving euros in Algeria is often more complex than it appears. While international payments are possible, individuals and freelancers frequently face structural barriers that affect how quickly, and how much, they actually receive.

Official vs. black market rates

One of the most significant challenges is the gap between official exchange rates and the informal “square” market rate. When euros are processed through official banking channels, they are converted at the government-regulated rate, which can be up to 30% lower in real purchasing power compared to the parallel market. This creates a hidden loss for recipients, especially freelancers and remote workers who depend on foreign income. While the official system is legal and secure, the financial trade-off often feels substantial and discouraging.

Also read: The ultimate digital bank account for freelancers in Algeria

Currency conversion pressure

In many cases, euros sent into Algerian bank accounts are automatically converted into Algerian Dinars (DZD) upon arrival. This means recipients may not have the flexibility to hold or manage their funds in foreign currency. For individuals working with international clients, this reduces financial control and limits the ability to save in a stable currency. It also exposes earnings to local inflation and exchange rate fluctuations, which can affect long-term financial planning and stability.

Bureaucracy and delays

Bank transfers in Algeria are often subject to strict regulatory checks, which can result in long processing times. It is not uncommon for payments to be delayed for weeks or even months while banks request documentation such as invoices, contracts, or proof of income source. Although these measures are designed to prevent fraud and ensure compliance, they can create frustration for recipients who rely on timely payments for living expenses or business operations. The uncertainty can also make cash flow planning difficult.

Limited receiving options

Another key challenge is the limited range of formal channels available for receiving euros. Many international payment platforms either do not operate fully in Algeria or offer restricted services. As a result, individuals often rely on traditional bank transfers, which are slower and less flexible. This lack of diversified payment infrastructure reduces choice and can push users towards informal or less secure alternatives. It also slows down the integration of Algerian freelancers into the global digital economy.

Receiving euros in Algeria is increasingly possible through digital platforms that simplify cross-border payments, reduce friction, and give users more control over how they access and convert funds.

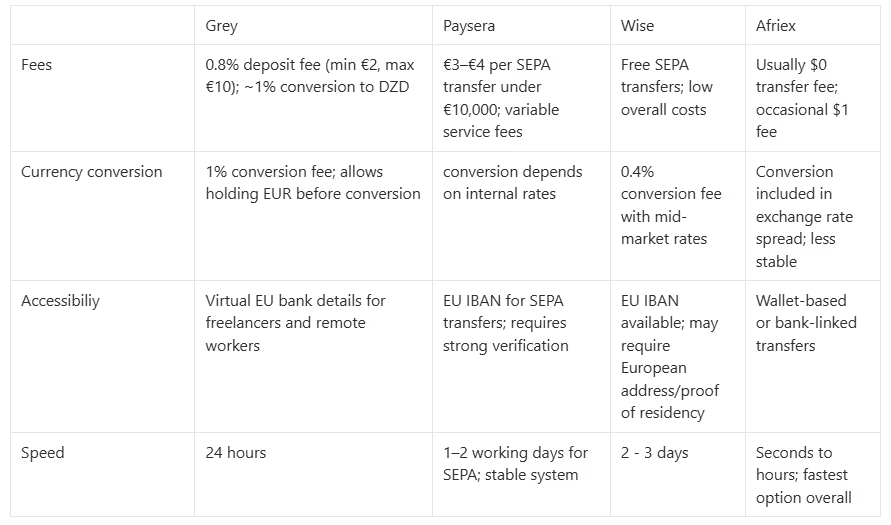

Grey

Grey allows users to receive euros into a digital account with virtual European banking details, making it suitable for freelancers and remote workers. Deposit channels such SEPA, and FPS typically attract a 0.8% fee, with a minimum charge of €2 and a maximum cap of €10, depending on transaction size. When converting euros to Algerian dinars, a 1% conversion fee is applied. This structure makes costs relatively predictable, while still giving users flexibility to hold euros before converting. Processing times are generally fast, supporting quicker access to funds compared to traditional banks.

Paysera

Paysera provides users with a European IBAN, enabling direct receipt of euros via SEPA transfers from clients or businesses across Europe. Incoming payments are generally charged between €3 and €4 for transactions below €10,000, making it cost-effective for moderate inflows. Users can keep funds in euros within the account, avoiding automatic conversion and giving more control over timing. However, additional fees may apply when withdrawing or transferring funds to other currencies. The platform is widely used for its stability, though verification requirements and compliance checks can extend onboarding time.

Wise

Wise supports multi-currency accounts, allowing users to receive, hold, and convert euros at low and transparent costs. SEPA transfers into Wise accounts are usually free, making it attractive for regular euro inflows. Currency conversion to Algerian dinars typically carries a low fee of around 0.4%, applied transparently using mid-market exchange rates. Users benefit from clear pricing without hidden spreads, helping them understand exact costs before transactions. However, full account functionality may require a European address and proof of residency, which can be a limitation for some users in Algeria.

Afriex

Afriex is designed for fast, low-cost international transfers, particularly across Africa and diaspora payment routes. Most transfers are free, though a small fee of around $1 may apply depending on the transaction type or corridor used. The platform focuses on speed, with many transactions processed almost instantly or within a few hours. Conversion rates are generally competitive, with costs embedded in the exchange spread rather than explicit charges. While convenient and accessible, features may vary based on user verification level and regional availability.

There are several practical situations in Algeria where holding or receiving euros becomes important, especially for individuals engaged in global work, financial planning, or cross-border transactions.

International expenses

You need euros when paying for international services such as online subscriptions, foreign tuition fees, software tools, or freelance platforms. Many global companies price their services in EUR or USD, making local currency conversion unavoidable. Holding euros helps reduce repeated conversion costs and gives more control over timing payments when exchange rates are favourable. It also ensures smoother payments without delays or card failures when transacting on global platforms regularly.

Portfolio diversification

Euros are useful for diversifying savings beyond the Algerian dinar, which can be exposed to inflation and currency volatility. By holding part of your income in euros, you spread financial risk across currencies. This approach is especially valuable for freelancers and remote workers who earn internationally and want to protect long-term purchasing power. It also provides financial stability during periods of local currency instability and supports better long-term planning for savings and investments.

Wealth preservation

In uncertain economic conditions, euros can serve as a stable store of value amid local currency fluctuations. Many individuals save in euros to preserve wealth and shield themselves from inflation pressures within the broader African economic environment. It also provides flexibility for travel, investment, or future relocation plans.

Also read: Algeria visa requirements for EU citizens

Optimising euro payments in Algeria requires more than just selecting a platform; it involves building habits that improve consistency and reduce financial leakage over time.

Hold euros before converting

Use platforms that allow you to store euros instead of forcing immediate conversion. This gives you more control over timing and helps you decide when exchange rates are most favourable. Instead of converting at the point of receipt, you can monitor market movements and convert when the rate works better for your income. Over time, this simple flexibility can make a noticeable difference in how much you actually retain from international payments, especially if you are earning consistently in euros.

Consolidate payments

Instead of receiving multiple small payments, try to combine invoices where possible. Each transaction often comes with a fee, and when payments are split, those charges repeat unnecessarily. By consolidating your earnings into fewer, larger payments, you reduce the number of times fees are applied. This improves overall cost efficiency and also makes it easier to track income, manage cash flow, and plan expenses more accurately. It is a small operational change that can significantly improve how much you keep over time.

Compare platforms regularly

Payment platforms are not static. Fees, exchange rates, and processing speeds can change, and new competitors often enter the market with better terms. Regularly reviewing your options ensures you are not locked into outdated or expensive systems. A platform that was cost-effective last year may no longer be the best choice today. By comparing periodically, you stay informed and positioned to move to better options that improve your overall earnings retention and reduce unnecessary losses.

Separate spending and savings

Keep a portion of your income in euros for stability while converting only what you need for local expenses. This approach helps you reduce exposure to currency fluctuations and protects your earnings from sudden naira depreciation. It also encourages better financial discipline by separating operational spending from long-term value storage. Over time, this balance gives you more control, smoother budgeting, and a stronger buffer against inflation risks.

Can I legally receive euros in Algeria through digital platforms?

Yes, you can receive euros in Algeria through regulated digital platforms and international transfer services. However, funds are often subject to local banking rules, documentation checks, and currency controls. While the platforms are legal, the way funds are converted or accessed may still depend on Algerian financial regulations.

Why do I lose money when receiving euros through banks in Algeria?

Losses usually come from currency conversion and exchange rate differences. Banks often apply the official rate, which is lower than the parallel market value. In addition, hidden service fees and automatic conversion to dinars reduce overall value. This gap creates a real difference in purchasing power for recipients.

Is it better to hold euros or convert immediately to dinars?

Holding euros is often more financially strategic, especially during inflation or currency instability. Euros maintain stronger global value compared to local currency fluctuations. However, immediate conversion may be necessary for daily expenses. The best approach depends on your financial goals, urgency of spending, and risk tolerance.

Why are international transfers sometimes delayed in Algeria?

Delays often result from strict compliance checks, anti-money laundering regulations, and documentation requirements. Banks may request invoices, contracts, or proof of income source before releasing funds. While these processes ensure security, they can significantly slow down payments, especially for freelancers who receive frequent international transactions.

Managing international payments from Europe is now easier for freelancers and remote workers in Algeria. Grey provides users with EUR accounts, complete with European banking details that allow clients to send payments as if they were making a local transfer within the SEPA network. This eliminates unnecessary friction and significantly simplifies cross-border transactions.

You can also manage multiple currencies, including EUR and GBP, all within the same platform, giving you greater control over your earnings. With competitive exchange rates and flexible conversion options, you can decide when and how to convert your funds.

Sign up on Grey and download the app to get your EUR banking details within minutes.

Grey charges fees on deposits, conversions, and withdrawals. Deposits via ACH, SEPA, or FPS incur a 0.8% fee (minimum $2/€2/£2, maximum $10/€10/£10). Currency conversions are charged at 1%, capped at $6. Withdrawal fees vary by currency: ₦35 for NGN, 0.5% for EUR/GBP (minimum €2/£2, maximum €10/£10), and $0.50-$0.65 for KES/UGX/TZS. Cross-border card transactions (non-USD purchases on a USD card) incur a 2% fee plus $0.50. Exchange rates are variable and include a margin over the mid-market rate. Always review fees and the rate before confirming a transaction. Visit grey.co/pricing for current rates.

.svg)

Back to top