A lot of people in Egypt have had this moment where they are trying to make sense of two different exchange rates at the same time. You check the official rate for the Egyptian pound against the US dollar or euro on your banking app or a quick Google search, then you hear what those same dollars or euros are trading for through black market. The gap feels too wide to ignore. For someone receiving money from abroad or trying to convert savings, the decision quickly becomes less about convenience and more about what value is actually preserved.

It often starts with a simple situation. A freelancer gets paid in dollars, a family receives support from abroad, or a small business imports goods and needs to convert currency. At the bank, the process is slow and limited and outside the system, the black market rate looks more attractive. However, it comes with uncertainty and risk that many people are no longer comfortable with.

This is where legal alternatives become important. Understanding how to access better regulated options helps you keep value, avoid risk, and move money more safely in everyday transactions

Also read: How Egypt is becoming a MENA hub for remote workers

Black market exchange rates in Egypt continue to attract users due to currency shortages, faster access, and stronger value than official banking channels today.

Black market exchange activity in Egypt offers significantly higher dollar-to-pound conversions compared with official bank rates. Limited foreign currency supply within formal institutions creates gaps that informal traders fill. Higher demand from businesses and individuals increases reliance on parallel markets.

Access becomes easier when official channels impose restrictions or caps on withdrawals. This difference in pricing encourages continued use of unofficial sources for currency exchange, especially during periods of economic pressure and constrained liquidity across the formal financial system.

Transactions within Egypt’s black market currency network are often completed faster than those processed through regulated banking systems. Formal banking procedures involve documentation, compliance checks, and approval stages that slow down access to foreign currency.

Black market networks reduce bureaucratic delays and prioritise immediacy for cash-based transactions. This efficiency becomes especially important during urgent financial needs, business payments, or travel-related currency requirements. Reliance on such channels increases when official systems are perceived as slow, restrictive, or unpredictable in delivery.

Remittance flows from Egyptians working abroad significantly influence demand for black market exchange services within Egypt. Higher informal exchange rates often encourage families to prefer unofficial transfer channels over regulated banking services.

This preference increases the real value received in local currency when funds are converted outside official systems. Diaspora communities rely on informal networks to maximise financial support sent to relatives facing economic pressure. Sustained remittance activity reinforces liquidity within the parallel market, keeping it active despite regulatory limitations.

Also read: How freelancers in Egypt earn and store foreign currency

Economic instability and regional disruptions limit the availability of foreign currency in official channels. Restricted supply forces businesses and individuals to seek alternative sources for essential imports and payments. Official banking systems often struggle to meet rising demand, creating widening gaps in access to foreign exchange. Persistent shortages sustain the relevance of parallel markets, which continue operating alongside regulated financial structures.

Understanding the risks of informal currency exchange shows how quickly convenience can turn into loss when you rely on unregulated systems, exposing you to fraud, insecurity, and financial uncertainty today

When you enter informal currency exchange networks, you often assume trust will protect you until something goes wrong. In a typical situation, you hand over cash or transfer funds without receipts or contracts, making it difficult to prove what was agreed later. If the dealer disappears or denies the transaction, you are left with no formal channel to pursue recovery. Legal systems cannot intervene in unregulated dealings, leaving you exposed to full financial loss even when the evidence feels convincing or emotionally certain.

Fraud becomes one of the most immediate dangers you face when dealing with informal currency brokers because transactions rely heavily on verbal agreements and reputation alone. You may be promised a favourable rate only to discover delays, excuses or outright disappearance of funds after payment. In many cases, hawaladars exploit urgency and lack of documentation to manipulate outcomes, leaving you powerless once money is handed over. The absence of verification systems increases vulnerability, making deception difficult to detect early or prevent entirely.

Cash -based transactions in informal currency markets often expose you to significant physical risk, especially when large amounts of money are carried or exchanged in unsecured environments. You may meet brokers in crowded public spaces or unfamiliar locations where surveillance is limited, increasing your vulnerability to theft or robbery. eEven seemingly routine exchanges can escalate quickly if information about cash movement is exposed. Without protection, informal systems lack security controls found in formal banking environments, leaving you dependent on personal caution alone, which may not always be sufficient.

Black market exchange systems can sometimes place you within broader financial networks linked to money laundering and illicit funding. Even if your intention is purely personal or business-related, you may unknowingly interact with intermediaries who operate outside regulatory oversight, exposing you to serious legal consequences. Authorities often monitor these channels for suspicious flows, meaning your transactions can become part of investigations without your awareness. This risk extends beyond financial loss into potential criminal implications, which can affect your reputation and long-term security, even after a single engagement period.

You may face regulatory penalties when engaging in informal currency exchange systems, because many governments treat unlicensed foreign exchange activity as a violation of financial laws. In practice, enforcement agencies may impose fines or restrictions on individuals found using such channels, and involvement can escalate consequences, especially when transactions are linked to unreported income or cross-border transfers. These measures are designed to discourage participation in unregulated markets while protecting formal financial systems.

Also read: How Egypt is becoming a MENA hub for remote workers

Banks and fintechs in Egypt are narrowing the foreign exchange gap through digital innovation, regulatory reforms, faster remittance systems, reducing reliance on informal markets and improving access to foreign currency

Increasingly, remittance flows from GCC countries reach households through instant fintech rails, allowing funds to arrive directly into your e-wallets or bank accounts within seconds instead of days. Instead of navigating traditional banking corridors, delays, and high fees, you experience immediate and more predictable access for everyday financial needs.

This shift reduces your dependence on informal channels, as regulated fintech platforms provide faster settlement, improved tracking, and clearer exchange rates across transactions. You benefit from stronger financial visibility while families receiving funds experience fewer delays and greater stability in household budgeting decisions over time now.

Regulators are increasingly licensing digital-only banks and RegTech providers to improve transparency and strengthen oversight across foreign exchange activity. In practice, this allows financial systems to track transactions more accurately while reducing opacity that previously surrounded currency movements. Digital banks integrate compliance tools that detect irregular flows, support real-time reporting, and align with central bank requirements for FX management.

This improves trust in formal channels and gradually shifts you away from informal exchange systems operating outside regulatory frameworks over time.

Banks in Egypt are progressively removing foreign exchange restrictions and cutting fees as liquidity conditions improve across the financial system. This reflects a shift in policy direction where previously tight controls were used to manage scarcity and stabilise demand. With improved foreign inflows and stronger banking reserves, access to official rates becomes easier for businesses and individuals. This reduces pressure on parallel markets and encourages you to rely on formal banking channels for currency exchange.

Across Egypt, digital payment platforms are increasingly giving you safer and cheaper ways to receive, hold, and convert foreign currency, reducing dependence on risky informal exchange systems while improving speed, transparency, and financial control in everyday cross-border transactions.

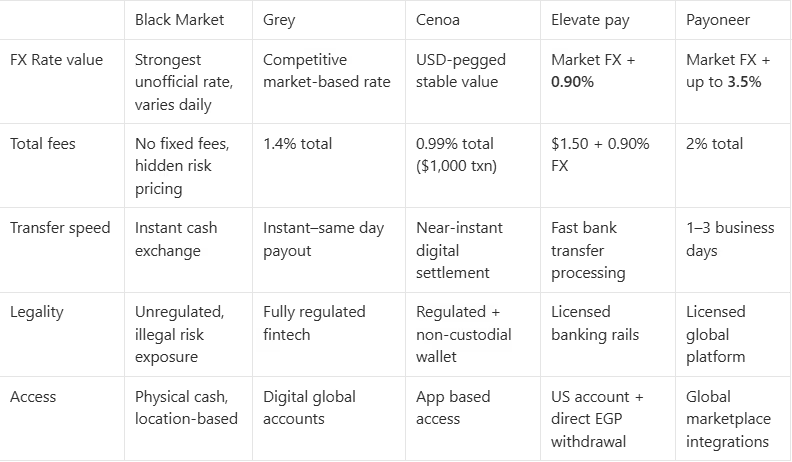

Grey targets freelancers and remote workers by providing virtual US, UK, and EU bank accounts that enable receipt of foreign currency payments seamlessly. It allows conversion into EGP at competitive rates and direct withdrawal into Egyptian bank accounts, making cross-border income more accessible for users. Total transaction cost averages around 1.4 percent, depending on payment method and corridor used, which remains significantly lower than traditional banking FX spreads in Egypt. This supports freelance global earnings stability, growth, and planning.

Cenoa is a non-custodial wallet enabling users to store savings in USD-pegged stablecoins and receive international payments efficiently. It also allows access to US bank account details for receiving funds, reducing dependence on high-cost banking intermediaries. Total fees are typically around 0.99 percent per 1,000 dollars, including 0.5 percent for receiving USD and 0.49 percent for conversion and withdrawal into EGP, making it a low-cost alternative for cross-border payments and savings management especially for users.

Elevate Pay provides US-based bank accounts for Egyptian residents, primarily serving remote workers and freelancers receiving international payments. It enables users to receive USD via ACH or wire transfers with minimal friction, offering free inbound transfers and competitive FX conversion into EGP. Withdrawal to Egyptian bank accounts is supported with a flat fee structure, typically around $1.50 plus exchange rate margin. Users benefit from transparent pricing, reduced intermediary costs, and improved access to official exchange rates compared to traditional banking systems in Egypt today, supporting digital income flows efficiently now.

Payoneer is a widely used global payments platform in Egypt, particularly among freelancers, agencies, and export businesses receiving international payments. It allows users to receive funds from global clients and marketplaces, though its fee structure is higher compared to newer fintech alternatives in the market. Currency conversion fees can reach around 3.5 percent, while withdrawal and transfer charges may add another 2 to 3 percent depending on method. Despite costs, it remains trusted for reliability, global reach, and established compliance infrastructure across international payment networks, especially for enterprise users today.

Here is a comparison table between black market exchange channels and legal fintech alternatives in Egypt, showing how each option differs

The biggest long-term risk is financial instability combined with legal exposure in Egypt. You face unpredictable rates, potential fraud, and lack of documentation, which can block dispute resolution, disrupt savings planning, and affect your ability to build consistent financial records.

Fintech platforms cannot fully replace banks, but they significantly reduce dependence on them for foreign exchange access. You still need banks for regulated savings, large transactions and loans. Fintech tools however improve speed, reduce costs, and simplify cross-border payments for everyday currency movement and income.

Fintech platforms often prove more cost-effective when fees, hidden risks, and exchange inconsistencies are taken into account. While black market rates may appear attractive, fintech services apply structured fees ranging from 0.5%-1.4%, of conversion fees, offering predictable and transparent costs.

Digital FX alternatives mainly benefit freelancers, remote workers, importers, and families receiving remittances. You gain faster access to foreign currency, lower transaction costs, and improved transparency, making it easier to manage international payments without relying on informal or unstable exchange systems.

Fintech platforms ensure transparency by showing real-time exchange rates, fixed fee structures, and transaction tracking from start to finish in Egypt. You see exactly what you send, what is deducted, and what arrives, removing hidden charges common in informal exchange systems.

Informal currency exchange in Egypt is no longer worth the risk, as regulated fintech alternatives now offer faster, safer, and more valuable services. Platforms like Grey stand out with transparent fees, highly competitive exchange rates, and seamless multi-currency accounts that let you receive, hold, and convert USD, GBP, and EUR with ease. Instead of uncertainty and exposure, you gain full control over your money with instant access and predictable costs.

Sign up or download the Grey app today and start moving money globally without stress.

Grey charges fees on deposits, conversions, and withdrawals. Deposits via ACH, SEPA, or FPS incur a 0.8% fee (minimum $2/€2/£2, maximum $10/€10/£10). Currency conversions are charged at 1%, capped at $6. Withdrawal fees vary by currency: ₦35 for NGN, 0.5% for EUR/GBP (minimum €2/£2, maximum €10/£10), and $0.50-$0.65 for KES/UGX/TZS. Cross-border card transactions (non-USD purchases on a USD card) incur a 2% fee plus $0.50. Exchange rates are variable and include a margin over the mid-market rate. Always review fees and the rate before confirming a transaction. Visit grey.co/pricing for current rates.

.svg)

Back to top