A first sale on a US marketplace often feels like a quiet breakthrough for many Kenyan sellers. An order comes in overnight, the dashboard updates, payment is marked as complete, and suddenly a product built or sourced in Kenya is reaching a customer thousands of kilometres away. On the surface, it feels like a simple loop: sell, ship, get paid in dollars.

But that clarity shifts once the payout begins its journey. A $500 order does not always arrive as a clean, predictable figure in Kenyan shillings. It moves through different processing stages, payout schedules, and conversion rates that can slightly reshape both timing and value before it reflects locally.

That moment changes the way many sellers see the process. The focus is no longer only on making sales, but on understanding how the money actually travels, what slows it down, and why the final amount can differ from what was first seen on screen.

This article explains how to receive payments from US marketplaces as a Kenyan seller, and what determines how your earnings move from sale to settlement in your local account.

Also read: Receiving USD from abroad while living in Kenya

Kenyan sellers face multiple challenges when receiving payments from US marketplaces that affect cash flow, costs, compliance, and overall business efficiency.

High transaction and conversion fees increase the cost of receiving international payments for Kenyan sellers. They often lose money due to intermediary bank charges, foreign exchange spreads, and withdrawal fees when converting USD to KES. These combined deductions reduce overall earnings and make pricing less competitive for small businesses relying on cross-border sales channels across global marketplaces today, frequently significantly.

Slow settlement times delay access to funds for Kenyan sellers using US marketplaces. Payments often take several business days and may be further delayed by banking holidays or intermediary processing systems. This creates cash flow pressure, making it difficult for sellers to restock inventory, pay suppliers or manage daily operational expenses effectively and consistently across international payment networks globally today.

Stringent KYC and regulatory compliance requirements make it difficult for Kenyan sellers to quickly access payment services platforms. Often, platforms demand detailed documentation such as business registration tax information and identity verification. This process can be slow and complex, leading to onboarding delays and occasional account restrictions, especially for small or first-time exporters entering us marketplaces within global ecommerce systems.

Currency fluctuation risk affects Kenyan sellers because the USD to KES exchange rate changes frequently. This volatility means the final amount received can be lower than expected, reducing profit margins. Sellers who price products in USD may struggle to predict earnings accurately, which makes financial planning and business forecasting more challenging over time for sustainability, especially in volatile market conditions today

Limited access to direct payment gateways forces many Kenyan sellers to rely on third-party payment providers. Most US marketplaces do not support direct deposits to local bank accounts or mobile money services like M-Pesa. This adds extra fees, processing delays, and dependency on external platforms, reducing efficiency and control over cash flow management for small cross-border sellers overall.

Minimum payout thresholds delay access to earnings for Kenyan sellers using certain payment service providers. Funds must accumulate before withdrawal, which can slow liquidity, especially for small sellers receiving frequent low-value transactions. This creates cash flow gaps and limits the ability to reinvest quickly into inventory, marketing, or operational needs within growing businesses, affecting long term business growth overall.

Also read: How freelancers in Kenya can receive payments from US, UK & EU clients

Setting up US marketplaces from Kenya requires structured steps across business registration, payments, and logistics to enable access to international selling platforms.

Register a US business entity by forming a legal structure such as an LLC or corporation through a registered state platform or service. This helps establish credibility, enables access to US marketplaces and payment gateways, and builds trust with customers and partners for smoother international business operations.

Set up US banking and payments by opening a business-friendly account through supported fintech providers or international banking partners. Connect this account to your marketplace seller profile to receive USD payments, reduce delays, and simplify currency conversion for smoother financial operations and faster access to sales revenue.

Register for an Amazon US seller account by visiting sell.amazon.com and completing the sign-up process. Provide required documents such as identity verification, business registration details, tax information, and bank account details. This ensures compliance, account approval, and access to the US marketplace for product listing and sales operations.

Fulfillment by Amazon (FBA) allows you to ship products in bulk from Kenya to Amazon US warehouses, where storage, shipping, returns, and customer service are managed by Amazon. Alternatively, use logistics partners like DHL or freight forwarders to transport goods efficiently, ensuring timely delivery and reliable cross-border fulfillment operations.

The best ways to receive payments from US marketplaces in Kenya include digital payment platforms, virtual accounts, and fintech solutions that simplify cross-border transactions and reduce fees significantly overall.

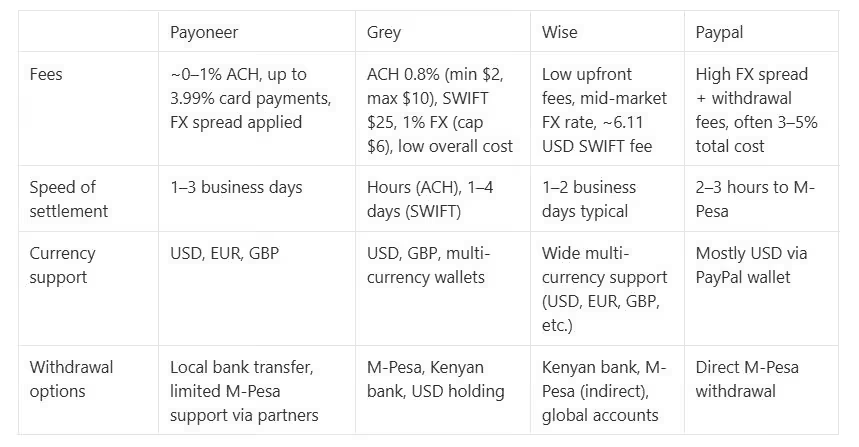

Payoneer is a highly recommended option for Kenyan sellers receiving payments from the US marketplaces. It provides virtual USD receiving accounts that work with platforms such as Amazon, Upwork, and Etsy. Funds are typically received via ACH transfers at a cost of up to 1% of the total payment and usually arrive within 1–3 business days. Receiving payments from other Payoneer users is free, while credit card payments may attract fees of up to 3.99% plus $0.49 per transaction. This makes it efficient for cross-border ecommerce sellers in Kenya today, overall convenient.

Grey is ideal for freelancers and sellers in Kenya who need fast and flexible access to US marketplace payments. It provides instant virtual UK and US account numbers, allowing users to receive payments quickly and convert funds to KES at competitive rates. Receiving USD via ACH costs 0.8% of the amount, with a minimum of $2 and a maximum of $10, while SWIFT transfers attract a flat $25 fee and take 1–4 business days. Withdrawals to M-Pesa cost $0.50 per transaction with instant processing, and bank withdrawals cost $0.65. Currency conversion charges are 1%, capped at $6, making it cost-effective overall. This supports scalable cross-border earning efficiency for users.

Wise is a reliable option for Kenyan sellers receiving US marketplace payments due to its transparent pricing and strong exchange rates. When receiving wire (SWIFT) payments into a Wise account, a fixed fee of 6.11 USD applies. Wise uses the mid-market exchange rate with a small upfront conversion fee, making it more cost-efficient than traditional banks. Converting funds to KES and withdrawing to M-Pesa is usually cheaper than bank transfers, with an example cost of about 12–18 USD for sending 1,000 USD. Wise also supports direct withdrawals to Kenyan bank accounts and mobile wallets, offering flexibility and predictable pricing for sellers. This makes it suitable for stable long-term international payment management in Kenya, an overall very effective solution.

PayPal-to-M-Pesa is one of the most common methods used by Kenyan sellers to receive payments from US marketplaces. It allows users to link PayPal accounts to M-Pesa for direct withdrawals. Funds typically arrive within 2–3 hours, making it a fast and convenient option for small and medium transactions. Although fees may be higher compared to other fintech platforms, its simplicity and widespread adoption make it accessible for many sellers managing cross-border income from US clients and marketplaces overall effective

Avoiding payment delays and high fees as a Kenyan seller requires smart systems, the right platforms, and disciplined financial practices to protect margins and improve cash flow overall

Grey is a strong option for Kenyan sellers because it combines fast access, low fees, multi-currency support and reliable cross-border payment control.

Regulatory protection and fund security: Grey operates under FINTRAC and FinCEN oversight, with customer funds held in segregated accounts at licensed partner banks. This keeps money separate from company operations, reduces risk, and ensures secure, compliant handling of international payments for Kenyan sellers.

Easy account setup for receiving payments: Grey allows quick creation of virtual USD or GBP accounts for receiving international payments. Sellers can share details and get paid like local transfers, reducing onboarding friction, simplifying cross-border transactions, and improving ease of receiving marketplace earnings efficiently.

Fast access to received funds: Payments reflect in Grey accounts within hours, depending on the sender’s bank, offering faster access than traditional SWIFT systems. This improves cash flow, reduces waiting time, and gives sellers better control over when to use or convert funds.

Transparent and competitive rates: Grey offers clear, upfront fees and competitive exchange rates with no hidden charges. This helps sellers retain more of their earnings, improves predictability, and ensures better financial planning when converting USD or GBP to Kenyan shillings for business use.

How long do US marketplace payments take to reach Kenyan accounts?

Payment speed varies by platform and method. ACH transfers typically take 1 to 3 business days, while SWIFT can take up to 5 days. Fintech providers like Grey often reflect funds within hours, improving cash flow predictability and operational efficiency for sellers.

Why do Kenyan sellers lose money during payment conversion?

Losses occur due to FX spreads, hidden bank charges, and conversion fees. Many banks convert USD to KES at non-competitive rates, reducing profit margins. Using multi-currency accounts and fintech platforms helps preserve value by offering mid-market exchange rates and lower fees overall.

Is it safe to use fintech platforms for international payments?

Yes, reputable fintech platforms are regulated under financial authorities such as FinCEN or equivalent bodies. They use segregated accounts and partner banks to safeguard funds. This structure ensures compliance, reduces fraud risk, and provides secure handling of cross-border marketplace payments for sellers.

What is the biggest mistake Kenyan sellers make with payments?

The biggest mistake is relying solely on traditional banks without comparing fees or exchange rates. This leads to high FX losses and delays. Not consolidating payments or ignoring fintech alternatives reduces profitability and slows cash flow for growing cross boarder businesses significantly overall.

For Kenyan sellers handling US marketplace payments, Grey provides a reliable edge through competitive exchange rates, multi-currency accounts, and fast cross-border transfers. It helps reduce hidden fees, improves access to funds, and simplifies global transactions.

You can easily get started by signing up or downloading the app to manage international payments.

Grey charges fees on deposits, conversions, and withdrawals. Deposits via ACH, SEPA, or FPS incur a 0.8% fee (minimum $2/€2/£2, maximum $10/€10/£10). Currency conversions are charged at 1%, capped at $6. Withdrawal fees vary by currency: ₦35 for NGN, 0.5% for EUR/GBP (minimum €2/£2, maximum €10/£10), and $0.50-$0.65 for KES/UGX/TZS. Cross-border card transactions (non-USD purchases on a USD card) incur a 2% fee plus $0.50. Exchange rates are variable and include a margin over the mid-market rate. Always review fees and the rate before confirming a transaction. Visit grey.co/pricing for current rates.

.svg)

Back to top