On a quiet evening in Algiers, a freelancer refreshes their phone, waiting. A client in London has just confirmed the payment, £450 for a completed project, sent and settled on their end. For a moment, there is relief. The work is done, the money is real, and it is on its way.

By morning, that certainty begins to shift. The question is no longer whether the money was sent, but what will actually arrive. Somewhere between the UK and Algeria, the payment passes through unseen steps, including conversion into dinars, with charges applied along the way, and the time stretches longer than expected. What started as £450 begins to feel less fixed.

This is the quiet tension many Algerians working with UK clients experience. Earning in pounds is one thing, but receiving that money intact is another. This article explores how to receive British pounds in Algeria, what factors determine the final amount, and how to navigate the process with greater control.

Also read: Hidden travel gems to explore in Algeria this summer

Receiving British pounds in Algeria can be more complex than expected, especially given local regulations and limited access to global financial systems that shape how money moves.

Strict currency controls

The Bank of Algeria maintains strict oversight on foreign currency, which affects how residents receive and manage GBP. Opening or operating foreign currency accounts is not always straightforward, and limits may apply to how much you can receive or hold. For consultants and freelancers, this can slow down growth and restrict flexibility. Understanding these controls helps you plan better, choose the right channels, and avoid unnecessary complications when working with UK clients.

Bank transfer delays and high fees

Receiving GBP through traditional bank transfers, especially via SWIFT, can be slow and costly. Payments may pass through intermediary banks, each taking a fee before the money reaches you. Local banks may also apply conversion charges at less favourable rates. This means the final amount received can be significantly reduced. For consultants, these delays and deductions can affect cash flow, making it important to explore faster and more cost-efficient alternatives.

Lack of access to global platforms

Access to widely used global payment platforms remains limited in Algeria, which creates challenges for those working with international clients. Services like PayPal have restrictions, and platforms such as Payoneer are not fully supported, reducing available options. This can make it harder to receive GBP seamlessly or integrate into global freelance ecosystems. However, being aware of these limitations allows you to explore emerging alternatives and find solutions that still enable you to work confidently with UK clients.

Also read: How to open US, UK and Euro bank accounts in Algeria

For Algerians working with UK clients, choosing the right platform can make a big difference in how quickly you receive your money and how much you actually keep.

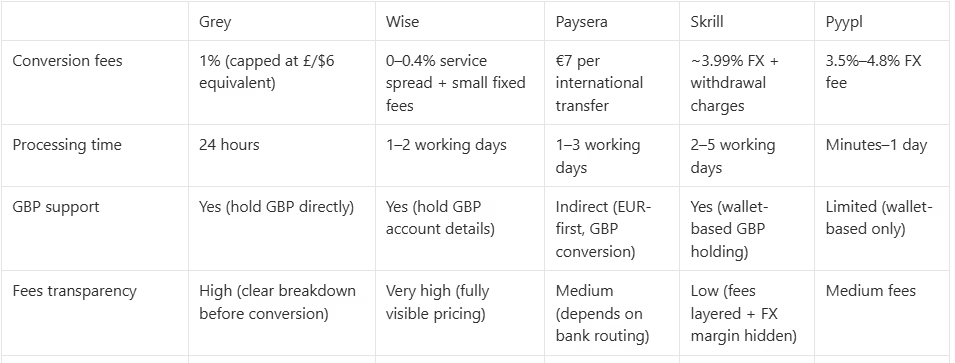

Grey

Grey is a strong choice for Algerian freelancers and consultants receiving GBP. It gives you access to GBP, USD, and EUR accounts, so clients can pay you like a local in the UK. Fees are relatively low, with about a 0.5% withdrawal fee (minimum £2, maximum £10) for GBP transfers. Sending to local Algerian accounts typically costs around $2.50, with funds arriving within five business days. This balance of speed, clarity, and flexibility makes it easier to manage international income without feeling overwhelmed.

Wise

Wise is known for its transparent pricing and use of real, mid-market exchange rates, which helps you avoid hidden losses. Receiving GBP via SWIFT usually comes with a fixed fee of about £2.16 per transaction. Transfers typically arrive within 1 to 5 working days, depending on the route. While Wise is reliable and widely trusted, some features like virtual cards may be limited in Algeria. Still, it remains a dependable option for consultants who value clarity and predictable costs.

Paysera

Paysera is a useful option if you are comfortable receiving funds in euros and then managing or converting them into pounds. It provides a secure digital account and works well for European transfers. International (SWIFT) transfers usually take 1 to 3 working days, with fees around €7 for non-EU transactions. If both sender and receiver use Paysera, internal transfers can be free. For Algerian users, it offers stability, though it may require a bit more planning when dealing directly with GBP.

Pyypl

Pyypl is a growing fintech option in the MENA region, offering virtual cards and international transfer features. It can be useful for managing online payments and subscriptions. However, there are ongoing costs to consider, including a monthly maintenance fee of $2.50 after the first three months. Foreign transactions attract fees between 3.5% and 4.8%, and withdrawing to a bank account costs around $5. While convenient, it is best suited for lighter usage rather than handling large, regular consulting payments.

Also read: How to receive payments from Upwork in Algeria in 2025

Choosing a payment platform as an Algerian consultant is not just about receiving money, it is about protecting value, ensuring speed, and reducing hidden costs that quietly affect your income over time.

Total cost

Many consultants only look at transfer fees, but the real cost includes exchange rate margins, conversion charges, and withdrawal deductions. A platform may advertise low fees but still reduce your earnings through poor FX rates. Always calculate the full cost of receiving £1,000 or $1,000, not just headline charges.

Speed and reliability of payments

Some platforms deliver funds within minutes, while others take several days due to compliance checks or bank routing. Delays can affect your ability to manage expenses or reinvest in your work. Choose platforms with consistent delivery times, not just occasional fast transfers.

Control over currency

A strong platform allows you to hold GBP, USD, or EUR instead of forcing immediate conversion. This control helps you convert when exchange rates are favourable, protecting your income from sudden fluctuations. Flexibility in timing often makes a significant difference to your real long-term earnings.

Grey helps Algerian users receive GBP from UK clients smoothly, without relying on traditional banks or facing long delays, hidden deductions, or complex cross-border processes.

Easy account setup for receiving GBP

With Grey, you get access to a virtual GBP account that allows UK clients to send you money like a local transfer. You simply share your account details, and payments are credited directly to your balance. This removes friction and makes receiving international payments feel simple, fast, and structured for everyday use.

Fast access to received funds

Once GBP is sent to your Grey account, it is quickly reflected in your balance, often within hours, depending on the sender’s bank. This speed helps you avoid long SWIFT delays common in Algeria. You can then hold your funds or decide when to convert, giving you more control over timing.

Transparent and competitive rates

Grey applies a clear pricing model when you receive and convert GBP, typically 0.8%, with capped fees for larger amounts. There are no hidden deductions from intermediary banks. This makes it easier for Algerian users to understand exactly what they receive and plan their finances confidently.

Here is a simple breakdown of how freelancers typically receive UK payments through Grey:

Start by signing up on Grey and completing the verification process. This usually includes identity checks and basic profile setup. Once approved, you gain access to a multi-currency dashboard that enables you to receive and manage international payments securely.

After verification, Grey provides you with virtual UK banking details, including a sort code and account number. These details function like a real UK bank account, allowing you to receive GBP payments directly from clients without needing a physical UK bank account.

You then share your UK account details with your client in London or anywhere in the UK. They can send payments normally through their bank, just like a local transfer. This removes cross-border friction and simplifies the payment process significantly.

Once your client sends the payment, it is credited to your Grey wallet. Processing is usually fast, depending on the sender’s bank. You can track incoming payments in real time, giving you visibility and control over your freelance income flow.

After receiving GBP, you can choose to hold it in your wallet or convert it into USD or EUR based on exchange rates. You can also withdraw to your local bank account, giving you flexibility over timing, currency strategy, and cash flow management.

Receiving British pounds in Algeria can be tricky, and many freelancers lose money not through big errors, but through small, repeated financial decisions that quietly reduce their total earnings over time.

Many freelancers focus only on transfer or platform fees, but overlook exchange rate margins, which often have a bigger impact on final earnings. Even a small difference in FX rates can reduce the real value of GBP payments significantly over time, especially for frequent international transactions.

Banks are often seen as the safest option, but they are usually the most expensive for receiving GBP. SWIFT transfers involve intermediary banks, extra charges, and processing delays, all of which reduce the final amount received and slow down access to funds.

Automatically converting GBP as soon as it arrives can lead to unnecessary losses. Exchange rates fluctuate constantly, and converting at the wrong time can reduce income. Holding GBP allows more control, giving freelancers the option to convert when rates are more favourable.

Many freelancers stick to a single payment platform out of convenience, without comparing alternatives. This can lead to avoidable losses, as different platforms vary in fees, FX rates, and processing speed. Comparing options regularly can help save 3%–5% per transaction.

Do I need a UK bank account to receive GBP?

No, you do not need a UK bank account. Grey provides you with virtual GBP account details that function like a real UK account. This allows Algerian users to receive payments directly from UK clients without opening foreign bank accounts or dealing with complex banking requirements.

How long does it take to receive GBP payments?

Most GBP payments arrive within a few hours to one or two business days, depending on the sender’s bank. Grey processes funds quickly once received. This is much faster than traditional SWIFT transfers, which can take several days or even weeks in some cases.

Is receiving GBP through Grey easier than a traditional bank in Algeria?

Yes, Grey removes the usual friction of international banking. Instead of waiting for SWIFT routing, intermediary banks, and paperwork checks, you receive GBP directly into a virtual UK account. It feels like local payment infrastructure, but for cross-border work, reducing delays, confusion, and rejected transfers common in traditional systems.

Can I keep my GBP or must I convert it immediately?

You can keep your GBP balance in Grey without converting it immediately. This gives you control over timing, allowing you to wait for better exchange rates. Many users prefer holding GBP to protect value and avoid converting during unfavourable market conditions.

Receiving international payments from UK clients is now much easier for freelancers and remote workers in Algeria with modern digital payment solutions. Grey provides users with virtual GBP accounts complete with real UK sort codes and account numbers. With these details, UK clients can pay you just like a local transfer within the UK, removing the usual friction of cross-border banking.

You can also manage USD and EUR payments on the same platform, giving you flexibility across multiple currencies. Funds can be converted at competitive rates when needed and accessed quickly through supported withdrawal options.

Sign up on Grey or download the app to get your GBP banking details within minutes.

Grey charges fees on deposits, conversions, and withdrawals. Deposits via ACH, SEPA, or FPS incur a 0.8% fee (minimum $2/€2/£2, maximum $10/€10/£10). Currency conversions are charged at 1%, capped at $6. Withdrawal fees vary by currency: ₦35 for NGN, 0.5% for EUR/GBP (minimum €2/£2, maximum €10/£10), and $0.50-$0.65 for KES/UGX/TZS. Cross-border card transactions (non-USD purchases on a USD card) incur a 2% fee plus $0.50. Exchange rates are variable and include a margin over the mid-market rate. Always review fees and the rate before confirming a transaction. Visit grey.co/pricing for current rates.

.svg)

Back to top