Earning across borders has become the reality for many freelancers, remote workers, and digital entrepreneurs, turning international payments into a routine part of daily business. As work moves online and clients spread across continents, traditional local banks struggle to keep up with the demands of global transactions.

Local banks were once enough when clients were nearby, and payments were straightforward, but slow transfers, hidden fees, and poor currency conversion have made them less practical for remote professionals. Today, offshore and international-friendly accounts offer a reliable, easy-to-open solution, helping freelancers manage payments efficiently and stay competitive in a global marketplace.

Before looking into options, it is worth clearing up what 'offshore' means in this context. An offshore bank account is simply a bank account held in a country other than where you live. If you are based in Brazil and open a USD account with a platform registered in the US or Canada, that is technically an offshore account. There is nothing secretive or illegal about it.

The term carries baggage from an era when offshore banking was associated with hiding wealth. That era is over. The Common Reporting Standard (CRS) and FATCA mean financial account information is now shared automatically between countries. If you hold an offshore account, your home country's tax authority likely knows about it. The practical implication is simple: declare the account, report any income, and comply with your local tax obligations. The benefit of offshore banking today is not secrecy. It is access: the ability to hold, receive, and spend in foreign currencies that your local bank does not support well.

You need an offshore account that is easy to open because global opportunities move fast, and when a foreign client is ready to pay, you cannot afford weeks of paperwork, complex compliance hurdles, or unrealistic deposit requirements slowing you down. A simple onboarding process lets you start receiving international payments quickly and keeps your cash flow steady from the start.

Accessibility becomes crucial when building a career independently without the backing of a large corporate structure. Many traditional offshore banks were designed for high-net-worth individuals, often requiring substantial deposits and stringent entry requirements. An easy-to-open alternative removes that barrier, giving you access to international banking without excessive financial thresholds or complicated corporate requirements.

Finally, flexibility matters in a rapidly changing global economy. An offshore account thatis easy to open lets you adapt to new markets, confidently accept cross-border contracts, and scale your freelance business without payment limitations holding you back.

Also read: How to open an offshore private bank account as a US citizen

For most freelancers and remote workers, a fintech multi-currency account is the practical equivalent of an offshore bank account, with a fraction of the setup friction. These platforms give you real foreign currency account details, virtual cards for spending, and the ability to hold and convert multiple currencies, all from your phone.

Grey provides multi-currency accounts in USD, GBP, EUR, and USDC, available to users across Africa, Europe, Asia, Latin America, North America, and Oceania. You get real US banking details (routing number and account number), plus EUR and GBP account details, so clients and platforms can pay you as if it were a local transfer in their country.

Account setup takes minutes. You download the app or sign up at grey.co, Complete KYC with a valid ID, and your account details are available immediately. There is no minimum deposit, no monthly maintenance fee, and no branch visit. Grey's virtual Visa card ($5 to create) supports Apple Pay and Google Pay in supported regions, so you can spend your foreign currency balance directly without converting first.

Grey also includes a built-in invoicing tool, stablecoin support (USDC), and naira/local currency withdrawals. For freelancers who need to receive, hold, convert, and spend across currencies, Grey covers the full workflow in one platform.

Setup time: Minutes. Fully online.

Minimum deposit: None.

Currencies: USD, GBP, EUR, USDC.

Card: Virtual Visa, $5 creation, Apple Pay, and Google Pay.

Available in: 78 countries (Africa, Europe, Asia, LatAm, North America, Oceania).

Best for: Freelancers, remote workers, and entrepreneurs in emerging and developed markets who need the fastest path to international banking.

Wise (formerly TransferWise) offers multi-currency accounts with account details in 10+ currencies, competitive mid-market exchange rates, and a debit card that works globally. Wise is well-established and trusted, with over 14 million users worldwide. For outbound transfers and currency conversion, its rates are among the best available.

However, Wise has limitations depending on where you are. The physical card is not available in all countries (including Nigeria). The platform has periodically adjusted its services in certain markets, and it has a strict policy against crypto-related transactions, which can result in account closure. Wise is also an Electronic Money Institution, not a bank, meaning your funds are held in safeguarding accounts rather than a bank account in your name.

Setup time: Minutes. Fully online.

Minimum deposit: ~20 GBP equivalent to activate account details.

Currencies: 40+ currencies held, 10+ with local account details.

Card: Debit card (not available in all countries).

Best for: Freelancers and remote workers who prioritise the lowest conversion cost on transfers and operate in countries where Wise is fully supported.

If you need a formal banking relationship, an account with deposit protection, or access to services that fintech platforms do not offer (lending, trade finance, formal bank references), a traditional offshore bank may be the right fit. These require more documentation and sometimes higher deposits, but they offer institutional stability and broader service portfolios.

A long-standing offshore bank in Belize offering multi-currency accounts (USD, EUR, GBP) with relatively simple opening requirements and online access. It is known for accommodating non-resident applicants and providing online banking once documentation (ID, proof of address) is submitted. Initial deposits and some fees apply, and wire transfers or debit card transactions may include conversion charges.

Eligibility: Open to non-residents globally. Requires notarised ID and proof of address for remote applications. An initial deposit is typically required.

Best for: Freelancers needing traditional offshore banking in a regulated Caribbean jurisdiction.

Jeton Bank operates as a digital international banking platform linked to the Belize banking infrastructure, designed for seamless cross-border payments and currency exchange. You can conduct international wire transfers and hold multiple currency sub-accounts online without frequent physical visits. The process typically involves standard KYC documentation and online verification.

Eligibility: Remote onboarding available. Standard KYC (ID, proof of address). Open to international users.

Best for: Digital-first users who want offshore banking with remote onboarding and multi-currency wire capability.

Statrys is a fintech-style multi-currency business account offering access to 11 major currencies with a straightforward digital setup. There is no hefty initial deposit, and receiving domestic HKD payments is free, though incoming international transfers and FX conversions incur modest fees. A small monthly account fee may apply if activity is low, but Statrys remains predictable with transparent pricing and online tools that integrate with marketplaces.

Eligibility: Fully online application. Primarily designed for businesses (requires company documents). Based in Hong Kong.

Best for: Small businesses and freelancers with a registered company who need multi-currency access through Hong Kong.

Aspire provides business banking and multi-currency accounts tailored for startups and freelancers, with an easy online-only signup. There is no minimum balance requirement, and tools include billing, invoicing, and expense management. Cross-border payments are supported through integrated FX and partner systems, though FX margins and transaction fees may apply depending on currency and transfer method.

Eligibility: Online onboarding. Requires business registration documents. Based in Singapore.

Best for: Startups and freelancers in Asia-Pacific who need business banking with built-in invoicing and expense tools.

Also read: Offshore bank accounts: What's realistic in 2026

OCBC is a major Singapore-based bank with multi-currency business and international accounts. It supports cross-border transfers with competitive flat fees and full-value remittances across key regions, ideal for freelancers or small businesses operating in Asia. Account setup usually involves more documentation and compliance than fintech options, but OCBC's established network, reliable digital banking platform, and ability to hold several currencies make it well-suited for long-term global banking.

Eligibility: Stronger documentation requirements. Best suited for applicants with Singapore connections or business activity in Asia.

Best for: Established businesses and professionals needing a long-term banking relationship in a major Asian financial centre.

A UK-based international banking arm that offers multi-currency accounts (GBP, EUR, USD) with online applications and mobile banking access. Monthly account fees apply unless you maintain a minimum balance, but these accounts include fee-free international payments (excluding correspondent bank charges) and standard global banking tools.

Eligibility: Online application. Requires a minimum balance to waive fees. More accessible for UK/EU residents or those with UK connections.

Best for: Those seeking an internationally recognised UK bank with formal account protection and multi-currency support.

Moneycorp Bank provides a secure multi-currency IBAN account that lets freelancers receive international payments from over 70 countries with simplified wiring and no receiving charges. Transfers and FX are managed through an intuitive platform with competitive exchange rates, and the multi-currency wallet reduces payment friction.

Eligibility: Fully digital sign-up. No complex offshore structure needed. Quick verification.

Best for: Global freelancers focused on receiving international payments and managing FX efficiently.

NatWest offers international current accounts geared towards customers with global financial needs. With online and app banking, fee-free international payments (excluding some correspondent costs), and debit card support, NatWest can serve freelancers holding accounts in pounds or other major currencies.

Eligibility: Eligibility criteria apply. Primarily suited for UK residents or those with existing NatWest relationships.

Best for: UK-based professionals needing international banking through an established high-street bank.

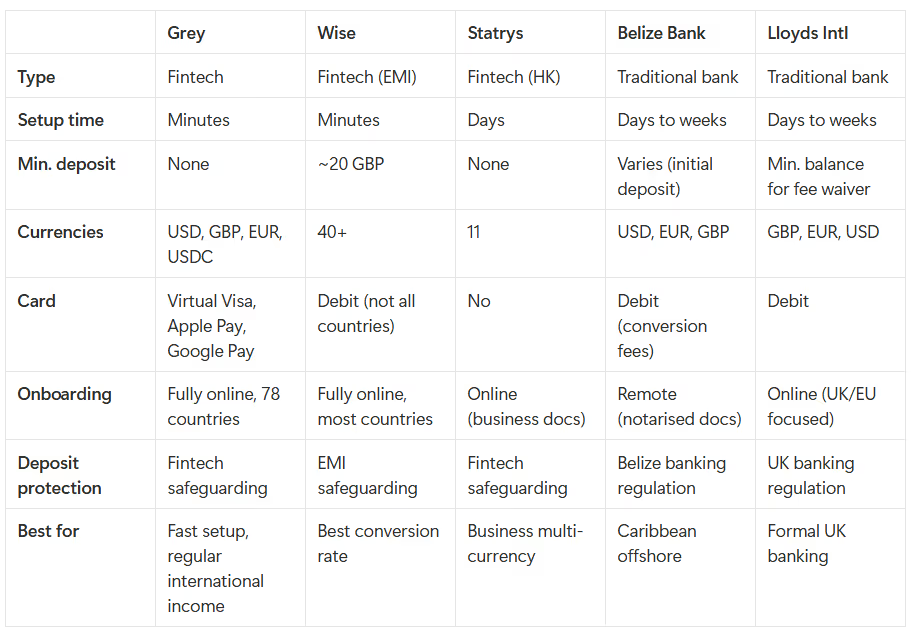

This table summarises the key differences across the fintech and traditional options covered above.

You are a freelancer or remote worker who needs to get set up fast and start receiving payments this week. A fintech multi-currency account is your best option. Grey (no minimum deposit, card with Apple Pay) or Wise (best conversion rates, 40+ currencies) will have you operational in minutes. No branch visit, no initial deposit, no waiting.

You run a registered business and need formal banking with invoicing and expense tools. Statrys (Hong Kong) or Aspire (Singapore) offer business accounts with integrated tools. Both are fully digital and do not require large initial deposits.

You need a long-term, traditional banking relationship in a major financial centre. OCBC (Singapore), Lloyds International (UK), or NatWest International (UK) provide institutional stability, deposit protection, and full-service banking. Expect more documentation and higher minimum requirements.

You want a Caribbean offshore structure for specific legal or planning purposes. Belize Bank International or Jeton Bank caters to non-residents with remote onboarding and multi-currency support. These are formal offshore banks in a traditional sense.

You want the lowest cost for occasional international transfers. Wise's mid-market exchange rate is hard to beat for single transactions. Use it alongside a primary account for day-to-day banking.

Yes. Holding a bank account in a country other than your own is legal in virtually every jurisdiction. The requirement is that you declare the account and comply with your home country's tax reporting obligations. Under CRS and FATCA, financial account information is shared automatically between countries, so there is no practical way to hide an offshore account even if you wanted to.

In most countries, yes. US citizens must file FBAR (FinCEN Form 114) if their foreign account balances exceed $10,000 at any point during the year. UK residents must declare foreign income on their tax return. Nigerian residents must declare worldwide income under the 2026 NRS rules. Check your home country's specific requirements.

It depends on the institution. Traditional banks may restrict applicants from certain jurisdictions. Fintech platforms tend to be more accessible. Grey, for example, is available in 78 countries. Wise operates in most countries, but with varying feature availability. Always check the platform's supported country list before applying.

An offshore bank account is held at a licensed bank in a foreign jurisdiction, with deposit insurance and full banking services. A multi-currency fintech account is typically held at an Electronic Money Institution (EMI) or a licensed fintech, with similar functionality (receiving, holding, converting, spending), but with different regulatory protections. For most freelancers, the practical difference is minimal. For large balance storage or formal banking requirements, a traditional bank offers more institutional protection.

It varies. Fintech platforms like Grey and Wise have no or minimal deposit requirements. Traditional offshore banks often require initial deposits ranging from $500 to $25,000 or more depending on the institution and jurisdiction. Check each bank's requirements before applying.

For pure speed and accessibility, fintech multi-currency accounts are the easiest. Grey's account setup takes minutes and requires no minimum deposit. Among traditional banks, Moneycorp and Jeton Bank offer the most streamlined digital onboarding.

Looking for the fastest way to go international? Sign up at grey.co and get your USD, EUR, and GBP account details in minutes. Available in 78 countries.

.svg)

Back to top