In Morocco, earning in US dollars is no longer limited to a few professions. Designers in Casablanca, consultants in Rabat, developers working remotely, and small business owners selling services abroad are now all being paid by US clients. The work is becoming more global, and dollar invoices are now part of everyday reality for many people.

But the experience of receiving that money is not always as smooth as earning it. A $500 payment can take different paths before it reflects locally, and what finally shows up in Moroccan dirhams does not always feel as straightforward as the invoice that was sent. Sometimes it arrives quickly, other times it moves through delays that make you check your account more than once.

That gap between what is sent and what is received is what makes the process worth understanding properly. This article explains the best way to receive US dollar payments in Morocco, what really happens behind each transfer, and how to approach it so you keep more of what you earn.

Also read: Best freelance platforms accessible from Morocco

Receiving US dollars in Morocco is now easier through digital platforms and global transfer services, but each option works differently depending on speed, cost, and how much control you want over your money.

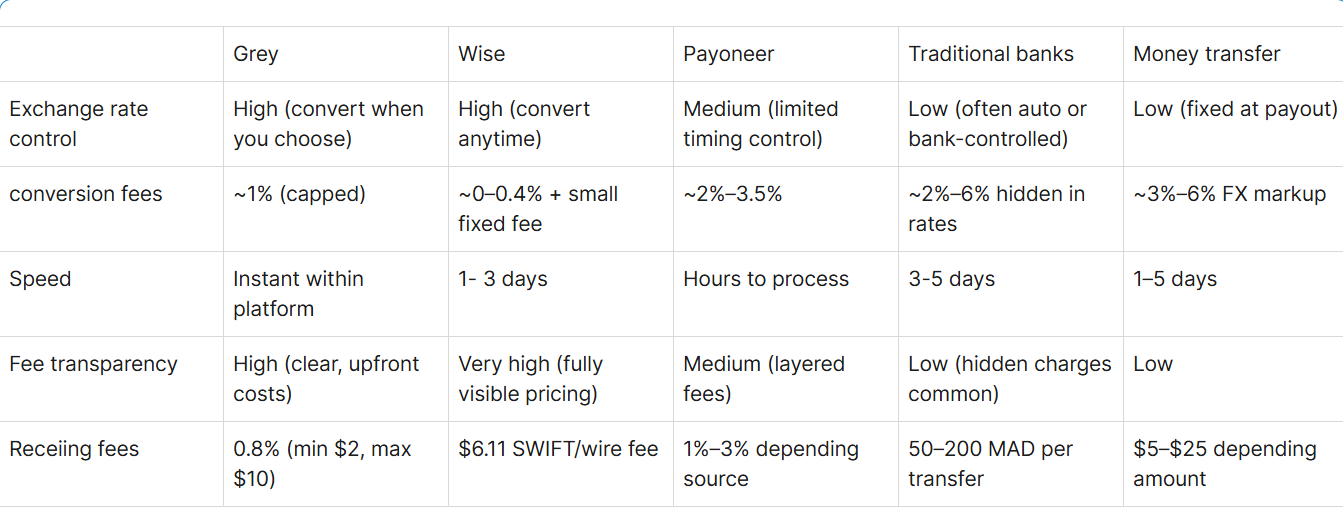

Wise

Wise is widely used because it gives you the real mid-market exchange rate when receiving USD in Morocco, which helps you avoid hidden losses. It is especially helpful for freelancers who want clarity on exactly what they are paid. Transfers into your account are usually charged a fixed fee of about $6.11 for wire or SWIFT payments, while ACH transfers are often free. Payments typically arrive within 1 to 5 business days, depending on the sender’s bank and route.

Grey

Grey is designed for users who want more control over how and when they convert their USD earnings. You receive dollars into a virtual account, then decide when to convert into Moroccan Dirhams based on exchange rates. This helps protect your income from poor timing. The receiving fee for ACH is 0.8%, with a minimum of $2 and a maximum of $10. Conversion costs are 1% capped at $6, and withdrawal to a Moroccan bank is a flat fee of $2.

Payoneer

Payoneer is popular among freelancers using global platforms like Fiverr, Upwork, and Amazon services. It allows you to receive USD from international clients and withdraw directly to your Moroccan bank account. However, the cost depends on how you are paid. Credit card payments attract around 3%, while eCheck payments are about 1%. There is also a yearly fee of $29.95 if the account is inactive, and withdrawal and conversion costs typically range between 2% and 3.5%.

Money Transfer Services (Western Union & Remitly)

Money transfer services like Western Union and Remitly are best when you need fast access to cash in Morocco. They are widely available through local agents such as Cash Plus and Wafacash, and you can often receive money within minutes. Bank deposits may take one to five business days, depending on the route. Fees vary based on the amount sent, and exchange rates include a built-in margin, which means you may receive slightly less than market value overall.

Traditional banking (SWIFT transfers)

SWIFT transfers are commonly used for formal international payments, but they are often slower and more expensive compared to digital platforms. Moroccan banks usually charge between 50 and 200 MAD for incoming transfers, while intermediary banks may also deduct additional fees along the way. Exchange rates often include a 2% to 6% margin, which reduces your final amount. Transfers typically take 3 to 5 business days, making this option better for large or occasional payments rather than regular freelance income.

Also read: Planning a remote-first career from Morocco

The black market for currency in Morocco often looks attractive on the surface because the exchange rate is higher than official channels. Many people feel they are getting “more value” for their euros or dollars when they convert informally. However, in simple economic terms, it comes with hidden risks that are not always visible at first.

There is no legal protection, no receipt trail, and no guarantee of fairness if something goes wrong. What looks like a better rate can quickly turn into uncertainty and financial exposure. For freelancers, students, and families receiving money from abroad, this can create instability rather than real gain.

The biggest issue is trust. Transactions are often cash-based and unregulated, meaning there is no formal system to resolve disputes. If money is lost, delayed, or miscounted, there is usually no recovery option. It also limits your ability to build a financial record, which is important for visas, loans, or business growth.

Over time, relying on the black market can disconnect you from formal financial systems, making it harder to scale income, prove earnings, or access safer global payment platforms that offer transparency and long-term financial security.

I know you want all your money, but let’s look at this like this. Imagine you run a small delivery service in Casablanca. Someone asks you to pick up a package, move it across cities, keep it safe, and deliver it on time. You would not do that for free. You would charge for fuel, time, risk, and the system you’ve built to make it reliable.

That is exactly how payment platforms work. Banks and platforms are not just taking money, while maintaining systems that move funds across countries, managing compliance checks, preventing fraud, and ensuring currencies are exchanged safely. These processes cost money, and that cost is shared across users. Without them, international payments would be slower, riskier, and less reliable for everyone involved.

The smarter approach is not avoiding fees completely, but understanding them deeply. When you know how much is lost to conversion, timing, and withdrawal, you start making better decisions. You choose platforms more carefully, you time conversions better, and you plan support to family in a way that does not drain your entire income at once.

Exchange rates work the same way. Platforms may not always give the exact market rate because they include a small margin to cover risk and operations. It is not always exploitation, it is the cost of making global money movement fast, secure, and dependable for everyday use.

Also read: Planning a remote-first career from Morocco

One of the most important but often overlooked parts of receiving USD in Morocco is how exchange rates and timing directly affect what you actually keep.

Exchange fluctuates

On paper, a $500 payment always looks the same. In reality, the value of that $500 can change depending on when it is converted, which platform is used, and how the FX rate is applied at the moment of withdrawal.

Exchange rates are constantly moving due to global market conditions, inflation trends, and currency demand. This means the Moroccan dirham value of your USD earnings is never fully fixed until the moment conversion happens. A small difference of 0.5% to 2% in exchange rates can significantly impact freelancers who regularly receive payments. Over a year, these small variations can add up to the equivalent of an entire project’s income lost without any visible “fee” being charged.

Timing matters

Timing also plays a major role. Converting immediately after receiving payment gives certainty, but it does not always give the best value. Holding USD for a short period can sometimes allow you to benefit from better rates, especially if your platform supports multi-currency wallets. However, holding too long without a strategy can also expose you to market drops, which is why balance matters.

Hidden FX costs

Another key factor is how platforms apply their own FX margins. Even when a service claims “real exchange rates,” there may still be small spreads included to cover operational costs. These are not always labelled as fees, but they function in the same way by reducing your final payout.

For freelancers in Morocco, understanding these dynamics is essential. It shifts the focus from simply “getting paid” to actually “maximising what you keep.” Over time, this awareness leads to better financial decisions, smarter platform use, and more predictable income from international clients.

Grey gives you a safe, structured way to receive international payments, helping you avoid delays, hidden charges, and the risks that come with informal or unreliable channels.

Why do different platforms charge different fees for the same payment?

Each platform operates on different infrastructure, partnerships, and risk models. Some prioritise speed, others focus on low cost or convenience. Fees also depend on currency routes and compliance requirements. That is why the same $1,000 transfer can arrive differently depending on the platform used.

Why do people still use the black market despite the risks?

Many people use the black market because the rate looks better at first glance. It feels like you are getting more value for your dollars or euros. But what is often missed is the lack of protection, no transaction record, and the hidden risk of loss if anything goes wrong during exchange.

How can I reduce losses when receiving international payments?

You reduce losses by understanding total cost, not just transfer fees. Compare exchange rates, choose platforms with transparent pricing, avoid unnecessary conversions, and time withdrawals wisely. Over time, small improvements in how you receive money can significantly increase your real take-home income.

Why does understanding exchange rates matter more than just focusing on the amount you are paid?

Because the value of your income changes depending on when and where you convert it. A good-looking payment can lose value quickly through poor timing or weak rates, meaning the same job can result in very different real earnings.

Receiving US dollars in Morocco does not have to be complicated or expensive. Grey offers a simple solution for freelancers, consultants, expats, students, and businesses who receive international payments. With USD accounts, you can receive money directly from US clients, hold your funds securely, and convert when rates are favourable. Transfers are fast, fees are low and transparent, and exchange rates are competitive, helping you keep more of your income. Whether for work or personal use, Grey makes receiving USD in Morocco easier, safer, and more efficient.

Sign up on the website or download the app, to manage your USD payments.

Grey charges fees on deposits, conversions, and withdrawals. Deposits via ACH, SEPA, or FPS incur a 0.8% fee (minimum $2/€2/£2, maximum $10/€10/£10). Currency conversions are charged at 1%, capped at $6. Withdrawal fees vary by currency: ₦35 for NGN, 0.5% for EUR/GBP (minimum €2/£2, maximum €10/£10), and $0.50-$0.65 for KES/UGX/TZS. Cross-border card transactions (non-USD purchases on a USD card) incur a 2% fee plus $0.50. Exchange rates are variable and include a margin over the mid-market rate. Always review fees and the rate before confirming a transaction. Visit grey.co/pricing for current rates.

.svg)

Back to top